Many people considering CeMAP hear stories about the exams being incredibly difficult, full of trick questions, or impossible to pass without years of financial experience. In reality, most of these beliefs come from misunderstandings rather than the qualification itself. Knowing what to expect can help you prepare more effectively and approach the exams with confidence.

Are CeMAP Exams as Hard as People Say?

The short answer is no, not for most learners.

CeMAP exams are challenging because they assess your understanding of mortgage advice, regulation and financial products. They are designed to ensure future mortgage advisers have the knowledge needed to work in a regulated profession. However, they are not intended to catch people out or require advanced mathematical ability.

Many learners pass by studying consistently, using quality learning materials and taking time to understand the topics rather than trying to memorise facts.

The difficulty often comes from the amount of information to learn rather than the complexity of the individual questions.

What Is CeMAP Actually Testing?

The Certificate in Mortgage Advice and Practice (CeMAP) is awarded by the London Institute of Banking & Finance (LIBF) and meets the educational requirements set by the Financial Conduct Authority (FCA) for individuals who want to provide regulated mortgage advice.

Rather than testing whether someone already knows the mortgage industry, the qualification assesses whether they have learned the knowledge needed to advise customers responsibly.

The exams cover areas such as:

- UK financial regulation

- Mortgage products

- Lending principles

- Property ownership

- Customer circumstances

- Ethical and professional responsibilities

The aim is to confirm understanding, not previous experience.

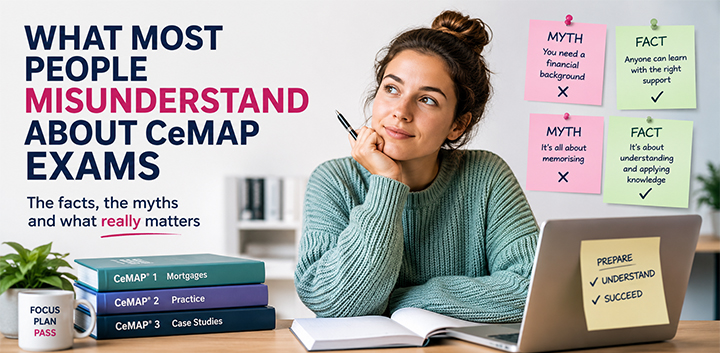

Misunderstanding 1: You Need a Financial Background

This is one of the most common myths.

Many people believe only bankers, accountants or experienced financial professionals can pass CeMAP. In reality, learners come from a wide variety of backgrounds.

Successful students include people who have previously worked in:

- Retail

- Hospitality

- Customer service

- Estate agency

- Administration

- Education

- Armed forces

- Self-employment

The qualification starts with the fundamentals before building towards more specialised mortgage knowledge.

Having experience in finance may make some topics feel more familiar, but it is not a requirement for success.

Misunderstanding 2: The Exams Are Designed to Trick You

Some learners worry that CeMAP exams are full of misleading questions designed to make people fail.

In reality, the exams are written to assess whether you understand the subject matter. Questions often present realistic situations where you need to apply your knowledge rather than simply remember a definition.

This sometimes creates the impression that questions are trying to catch you out.

More often, the challenge is reading carefully and understanding exactly what the question is asking.

Taking time to practise multiple-choice questions and learning how questions are structured can make a significant difference.

Misunderstanding 3: You Have to Memorise Everything

Another common concern is that success depends entirely on memorising hundreds of pages of information.

While some factual knowledge is important, CeMAP places considerable emphasis on understanding principles.

For example, knowing why regulation exists, how different mortgage products work or why affordability assessments matter will often help you answer several different questions.

Learners who focus only on memorising individual facts can sometimes struggle when questions are presented in a different way.

Understanding the subject is usually more valuable than learning isolated facts by heart.

Misunderstanding 4: If You Fail Once, You'll Probably Never Pass

Failing an exam can feel disappointing, but it does not mean someone is unsuited to becoming a mortgage adviser.

Many successful advisers have needed more than one attempt at part of their qualification.

Sometimes learners discover they underestimated the amount of preparation required. Others simply experience exam nerves or identify areas where they need more revision.

A previous unsuccessful attempt often helps learners understand how the exam works, making their future preparation more focused.

One result does not define your ability.

Misunderstanding 5: You Need to Be Brilliant at Maths

People are often surprised to learn that CeMAP is not a maths qualification.

You should be comfortable with basic numerical concepts, percentages and interpreting financial information, but the qualification does not involve advanced mathematical calculations.

The emphasis is on understanding mortgage principles and applying financial knowledge appropriately.

For many learners, reading comprehension and understanding regulation are more significant challenges than mathematics.

Misunderstanding 6: Studying Longer Always Means Better Results

It can be tempting to think that spending hours reading every evening is the best way to prepare.

In practice, quality often matters more than quantity.

Many learners benefit from:

- Studying in shorter, focused sessions

- Regular revision rather than cramming

- Practising sample questions

- Reviewing weaker topics

- Using a mixture of books, videos and tutor support

Learning effectively is usually more valuable than simply studying for longer.

Misunderstanding 7: Everyone Finds the Same Parts Difficult

There is no single section that every learner struggles with.

Some people find regulation straightforward but need more time with mortgage products.

Others quickly understand lending principles but take longer to remember legal terminology.

Your previous experience, study style and confidence all influence which topics feel easier or harder.

Comparing yourself with other learners is rarely helpful because everyone’s strengths are different.

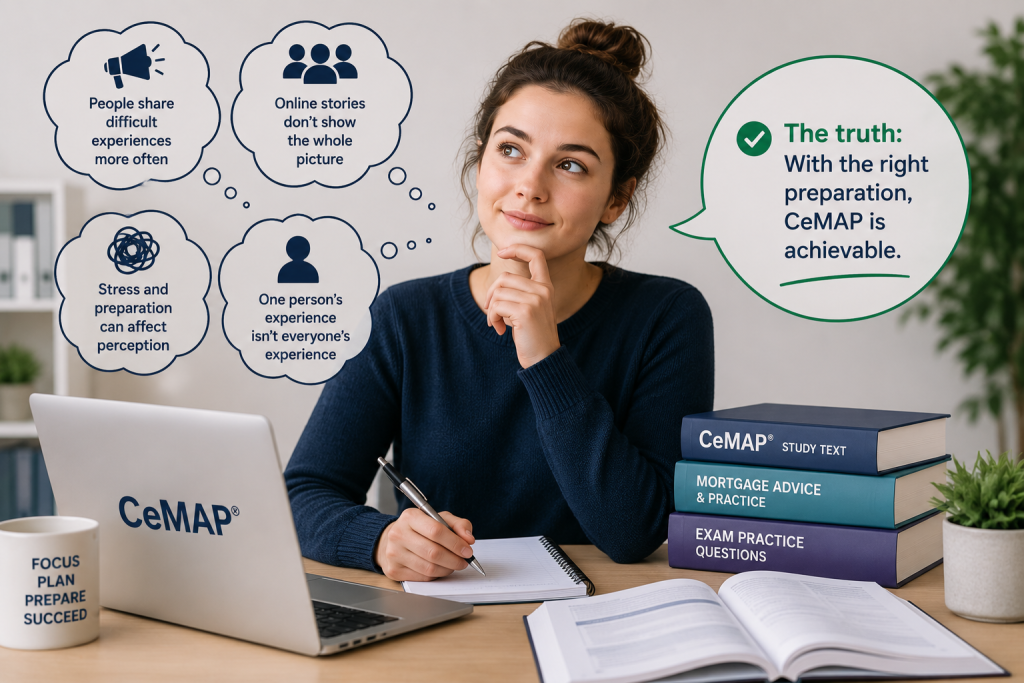

Why Do So Many Stories Make CeMAP Sound Difficult?

People naturally tend to share challenging experiences more often than straightforward ones.

Someone who found the exams stressful is more likely to talk about it than someone who quietly revised, passed and moved on.

Online discussions can also unintentionally exaggerate the difficulty. One learner’s experience may be influenced by limited preparation, outdated study materials or personal circumstances.

That does not mean the exams are easy, but it does mean individual stories do not always represent what most learners experience.

Looking for balanced, reliable information can help you build realistic expectations.

What Helps Learners Feel More Confident?

Confidence usually grows from preparation rather than luck.

Many successful learners:

- Follow a structured study plan

- Break large topics into manageable sections

- Use accredited learning resources designed for CeMAP

- Complete practice questions regularly

- Revise consistently instead of relying on last-minute study

- Ask questions whenever something is unclear

Using learning materials from an accredited LIBF Learning Support Provider can also help ensure your resources are aligned with the current CeMAP syllabus and learning outcomes.

Good preparation makes the exams feel far more manageable.

Should You Be Worried About Exam Nerves?

Feeling nervous before an exam is completely normal.

Even well-prepared learners often feel anxious because they care about doing well.

Simple preparation strategies can help reduce unnecessary stress, including:

- Getting enough rest before the exam

- Arriving with plenty of time

- Reading each question carefully

- Avoiding rushing through the paper

- Focusing on one question at a time

Confidence usually comes from knowing you have prepared properly rather than trying to eliminate every feeling of nervousness.

Is CeMAP More About Understanding Than Memory?

Yes.

Although some factual recall is required, CeMAP is largely about demonstrating that you understand how mortgage advice works within the UK’s regulated environment.

Understanding relationships between topics often makes revision easier.

For example, when you understand why affordability assessments, customer protection and regulation all work together, individual facts become easier to remember because they fit into a wider picture.

This deeper understanding is also much more useful once you begin working as a mortgage adviser.

Final Thoughts

Most misunderstandings about CeMAP exams come from second-hand stories rather than the qualification itself.

The exams are designed to assess knowledge and understanding, not to discourage people from entering the profession. They require commitment, consistent study and good preparation, but they do not require years of financial experience or exceptional academic ability.

Approaching CeMAP with realistic expectations is often one of the biggest advantages a learner can have. Instead of worrying about the myths, focus on building your understanding step by step, using reliable study materials and giving yourself enough time to prepare.

For many people, CeMAP is challenging but entirely achievable with the right approach.

Looking for training support?

We offer CeMAP training for learners working towards a career in mortgage advice. Our courses follow the London Institute of Banking & Finance syllabus and are designed to support understanding of mortgage regulation and advice requirements.

Explore our accredited CeMAP training courses

> Futuretrend Financial Training