Studying for CeMAP (Certificate in Mortgage Advice and Practice) can feel overwhelming at first.

The official syllabus from the London Institute of Banking & Finance (LIBF) and the regulatory material linked to the Financial Conduct Authority (FCA) are detailed for a reason. They are designed to define what mortgage advisers need to know before giving regulated advice.

But there is a big difference between a syllabus that lists what you must learn and a revision guide that helps you actually understand it.

A good CeMAP revision guide should take a large, technical syllabus and turn it into something manageable, clear and easier to remember.

What Is a CeMAP Revision Guide?

A CeMAP revision guide is a study resource designed to explain the official syllabus in simpler language.

It should:

- Cover all examinable topics

- Break complex ideas into smaller sections

- Use plain English instead of technical jargon

- Highlight key facts and definitions

- Help learners prepare for the exam efficiently

The purpose of a revision guide is not to replace the official syllabus. Its job is to make that syllabus easier to understand and revise.

That distinction matters.

The official syllabus tells you what you need to know. A revision guide should help you understand how to learn it.

Why the Official CeMAP Material Can Feel Difficult

The CeMAP qualification is the industry-standard mortgage advice qualification in the UK. It is awarded by the London Institute of Banking & Finance and meets the FCA’s education requirements for advisers who want to provide mortgage advice.

That does not mean the study material is always easy to digest.

Many learners struggle because the content includes:

- Legal and regulatory terminology

- Detailed product rules

- Large amounts of factual information

- Technical definitions

- Long paragraphs with little explanation

If you are new to financial services, this can feel like being handed a dictionary and told to memorise it.

That is where revision guides become useful.

Dense Material vs Simplified Material

Not all study resources are created in the same way.

Dense Material

Dense material often:

- Uses formal wording taken directly from regulations

- Includes long blocks of text

- Introduces several concepts at once

- Provides limited explanation

- Assumes prior knowledge

This approach may be technically accurate, but it can be hard to absorb.

Simplified Material

A well-written revision guide should:

- Explain one idea at a time

- Use examples to illustrate concepts

- Translate technical terms into everyday language

- Highlight the most important facts

- Summarise key points clearly

For example, rather than simply stating that a mortgage intermediary must comply with FCA disclosure requirements, a simplified guide might explain:

“Mortgage advisers must tell clients who they are, what service they offer and how they are paid before giving advice.”

The rule remains the same, but the explanation is much easier to understand.

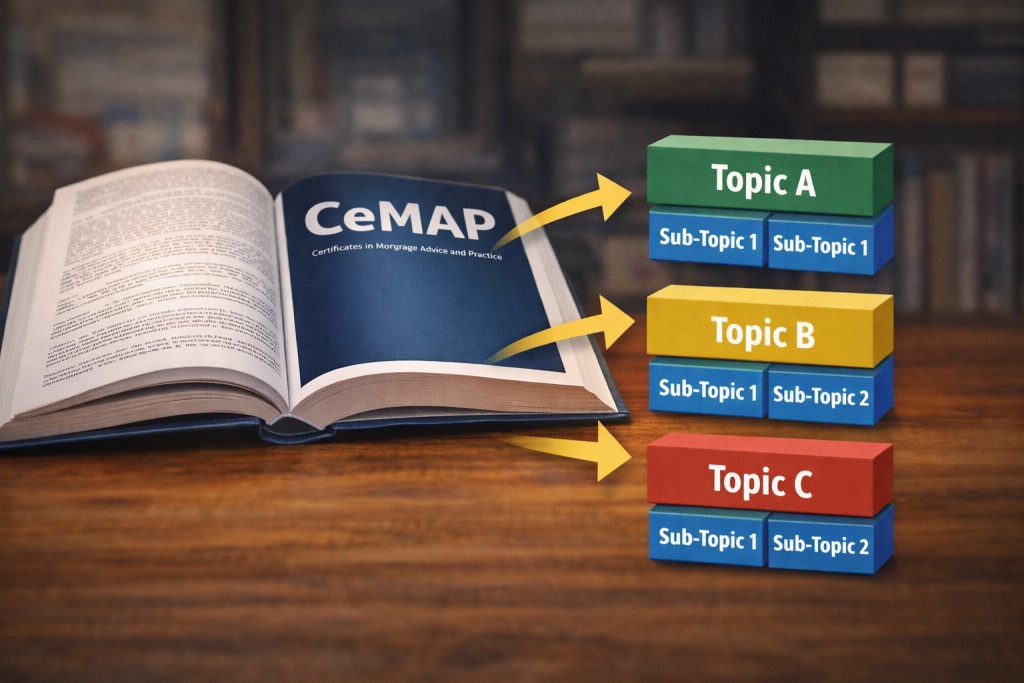

How Good Revision Guides Break Down Topics

The best CeMAP study guides divide each topic into smaller, logical chunks.

Instead of presenting an entire chapter on mortgage regulation in one go, they break it into sections such as:

- Who regulates mortgage advice

- What advisers are allowed to do

- Required disclosures

- Complaints procedures

- Consumer protection rules

This step-by-step structure helps learners build understanding gradually.

It is much easier to remember five short explanations than one long wall of text.

Examples of Topics That Benefit from Simplification

Some CeMAP topics are particularly suited to simplified explanations.

Regulation and Compliance

Rules and definitions can sound intimidating, but they become clearer when explained in practical terms.

Mortgage Products

Understanding the difference between repayment, interest-only, fixed-rate and tracker mortgages is easier when each product is compared side by side.

Calculations

Concepts such as loan-to-value (LTV) and debt-to-income ratios are more memorable when shown with worked examples.

Protection Products

Life cover, critical illness and income protection are easier to grasp when their purpose is explained in plain English.

What to Look for in a Good CeMAP Revision Guide

If you are comparing study materials, there are several signs of quality.

Clear, Simple Language

The guide should explain technical terms without making them sound more complicated than they are.

Logical Structure

Topics should be organised in the same order as the syllabus so you can track your progress.

Bite-Sized Sections

Short sections are easier to review and revisit.

Key Point Summaries

Important facts should be clearly highlighted.

Practical Examples

Examples help turn abstract concepts into real-world situations.

Practice Questions

Questions test understanding and reveal weak areas.

Up-to-Date Content

Mortgage regulation changes over time, so materials should reflect the current syllabus.

Are CeMAP Revision Guides Enough?

For many learners, a good revision guide is enough to understand the syllabus and prepare effectively for the exams.

However, revision guides work best when used alongside:

- Practice questions and mock exams

- The official syllabus specification

- Additional explanations for difficult topics

- A structured study plan

Think of a revision guide as the core of your study materials rather than the only tool you use.

If your guide covers the full syllabus clearly and you complete enough question practice, it may be all you need academically.

If you struggle with exam technique or motivation, you may benefit from extra support such as workshops, tuition or structured learning programmes.

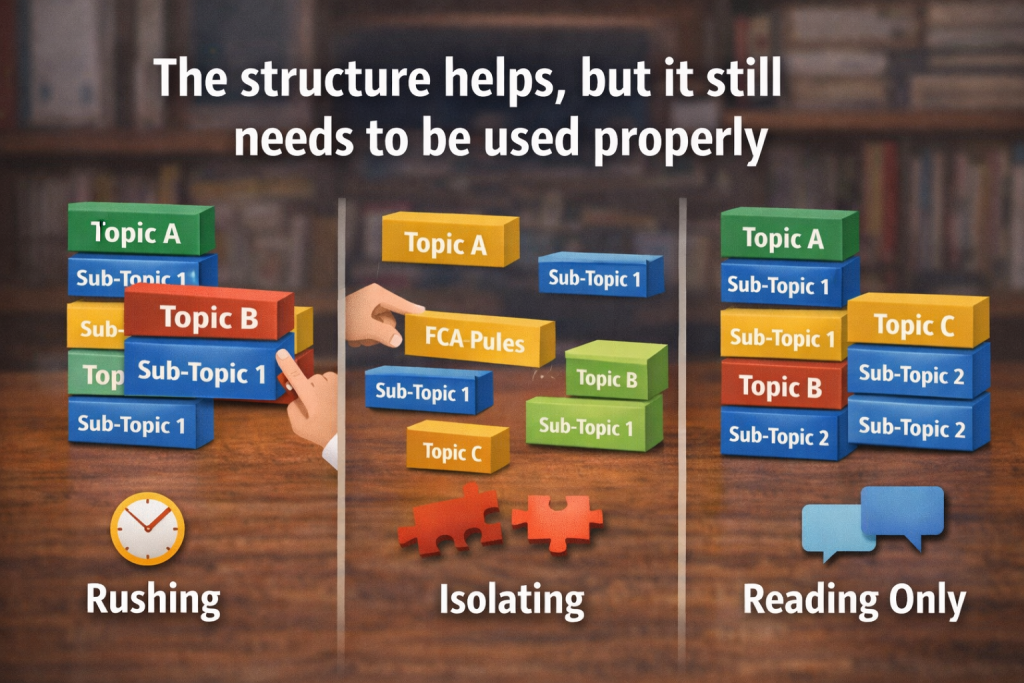

How to Use CeMAP Revision Guides Effectively

Even the best guide is only useful if you use it properly.

1. Start With the Syllabus

Understand what each unit covers so you know what the exam expects.

2. Read in Small Sections

Focus on one topic at a time.

3. Make Your Own Notes

Writing summaries in your own words improves retention.

4. Test Yourself Regularly

Use practice questions after each chapter.

5. Revisit Weak Areas

Spend extra time on topics that consistently trip you up.

6. Use Spaced Revision

Review topics several times over a period of weeks rather than cramming.

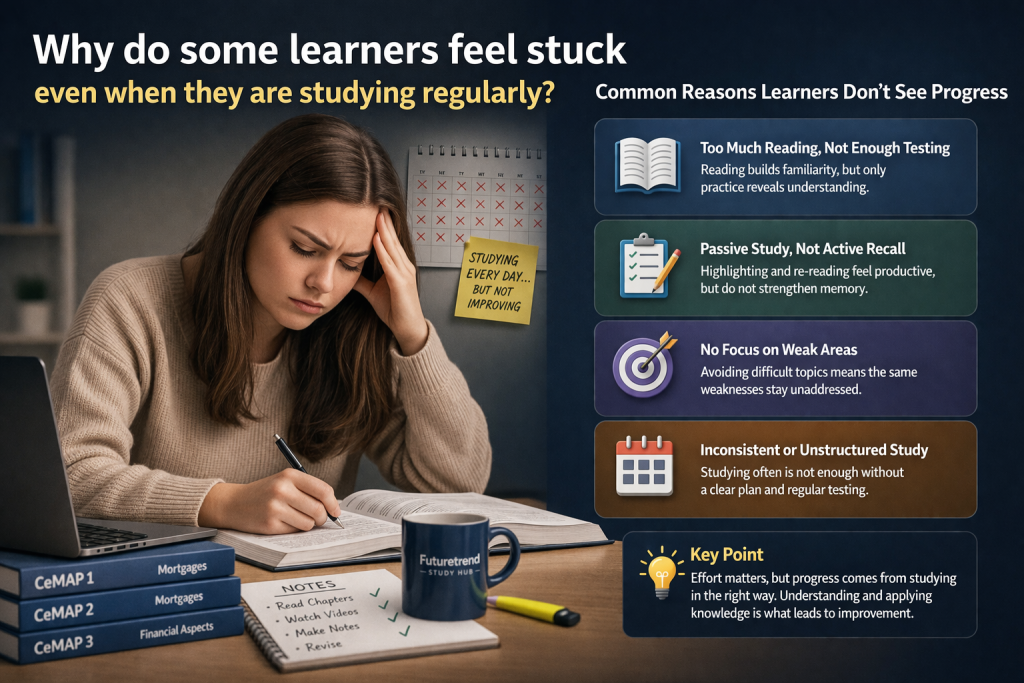

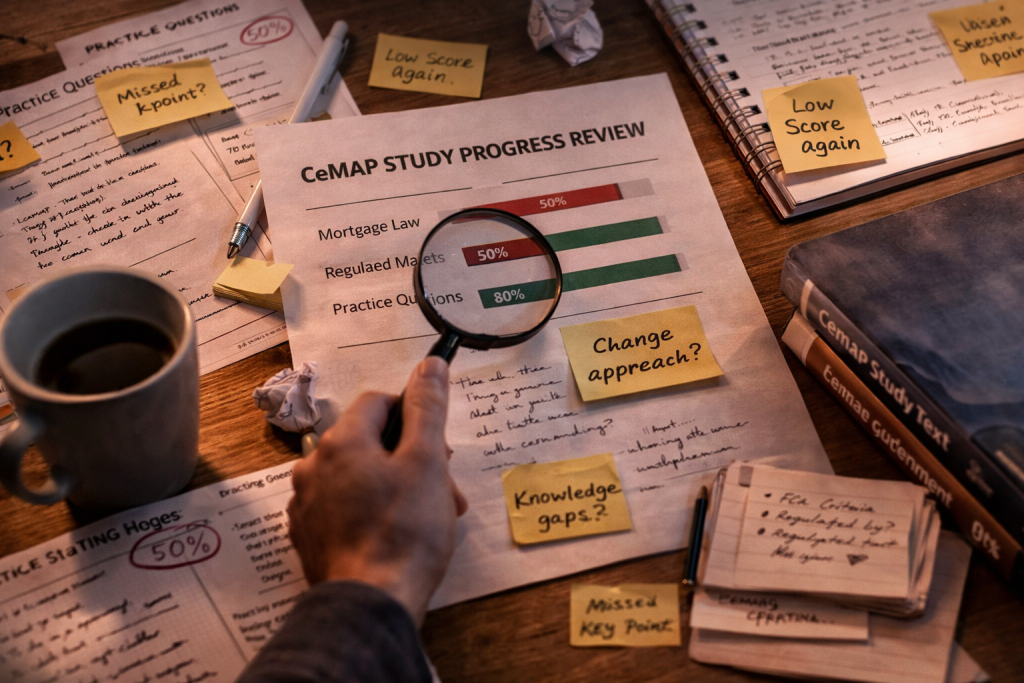

Signs Your Current Materials May Not Be Working

You may need better revision guides if you find that:

- You keep rereading the same pages

- The explanations feel overly technical

- You understand the words but not the meaning

- You struggle to connect concepts together

- Your mock exam scores are not improving

Good study materials should make learning feel clearer, not more confusing.

Why Simpler Explanations Improve Exam Performance

The CeMAP exams test understanding as well as recall.

If you genuinely understand a topic, you are more likely to:

- Interpret questions correctly

- Spot distractor answers

- Apply knowledge to scenarios

- Retain information longer

Simplified study materials help build this understanding by reducing unnecessary complexity.

That does not mean oversimplifying the content. It means presenting it in a way that is easier to learn.

Can Revision Guides Replace the Official Textbooks?

Revision guides are designed to support learning, not to change the syllabus.

A comprehensive guide should cover the same topics as the official material, but in a more accessible format.

Many learners find they understand concepts faster when they start with simplified notes and then refer to official wording only when needed.

This approach saves time and reduces frustration.

Choosing the Right Study Materials for Your Learning Style

Different learners prefer different formats.

You may find it helpful to use:

- Printed study guides for focused reading

- Digital guides for quick searching

- Audio lessons for learning on the move

- Flashcards for memorising key facts

- Mock exams for exam practice

The best resources are the ones you can use consistently.

Final Thoughts

CeMAP revision guides should make the syllabus easier to understand, easier to remember and easier to revise.

A good guide will:

- Cover the full syllabus

- Use clear language

- Break topics into manageable sections

- Include examples and summaries

- Support effective exam preparation

If your current materials feel dense or confusing, it may not be the syllabus that is the problem. It may simply be the way the information is presented.

The right revision guide turns a daunting qualification into a structured learning journey that feels far more manageable.

Looking for training support?

We offer CeMAP training for learners working towards a career in mortgage advice. Our courses follow the London Institute of Banking & Finance syllabus and are designed to support understanding of mortgage regulation and advice requirements.

Explore our accredited CeMAP training courses

> Futuretrend Financial Training