When people ask “What support do you get with CeMAP?”, they are usually trying to work out one thing: will they be left to figure it all out alone, or guided properly through it?

Study support is not just about having materials. It is about how you are helped to understand, apply, and stay on track while working towards a regulated qualification.

This matters because CeMAP is not simply about memorising facts. It is about understanding how mortgage advice works in practice, within rules set by the Financial Conduct Authority (FCA). The way support is delivered can shape how confident and prepared you feel when you move into the role.

What does “study support” mean for CeMAP?

Study support refers to the guidance, structure, and feedback available to help you progress through the CeMAP qualification.

In practical terms, it usually includes:

- Access to tutors or subject specialists

- Structured learning materials and study plans

- Feedback on practice questions or assessments

- Help with understanding difficult topics

- Support with exam preparation

Good support makes the learning process clearer and more manageable. It reduces the risk of getting stuck or misunderstanding key concepts.

Poor or limited support can leave learners unsure whether they are on the right track, especially if they are new to financial services.

What support do you get with CeMAP?

The support you receive with CeMAP depends on how you choose to study, but effective support usually includes three core elements: access to tutors, structured learning, and meaningful feedback.

Each of these plays a different role in helping you progress.

How important is tutor access?

Tutor access is one of the most important parts of CeMAP study support.

A tutor is not there just to answer questions. They help you:

- Break down complex topics

- Explain how rules apply in real scenarios

- Clarify areas where textbooks feel unclear

- Keep your understanding aligned with exam expectations

For example, topics such as regulation, affordability, and mortgage products can seem straightforward at first, but often involve nuance. A tutor can explain not just what the rule is, but why it matters and how it is applied.

Good tutor support usually means:

- You can ask questions when needed

- Responses are clear and relevant

- Explanations are practical, not just theoretical

Without this, learners often rely on guesswork or spend too long trying to interpret material on their own.

What does structured learning actually look like?

Structure is what turns a large amount of content into something manageable.

CeMAP covers multiple modules, each with its own topics, terminology, and regulatory context. Without structure, it is easy to feel overwhelmed.

Effective structured support usually includes:

- A clear study plan or pathway

- Content broken into manageable sections

- Suggested timelines (without rigid deadlines)

- Logical progression from basic to more complex topics

Structure helps you answer key questions while studying:

- What should I focus on today?

- What comes next?

- Am I covering everything I need?

It also reduces the risk of skipping important areas or spending too long on less relevant details.

Importantly, structure should guide you, not pressure you. Everyone learns at a different pace, and good support allows flexibility while still providing direction.

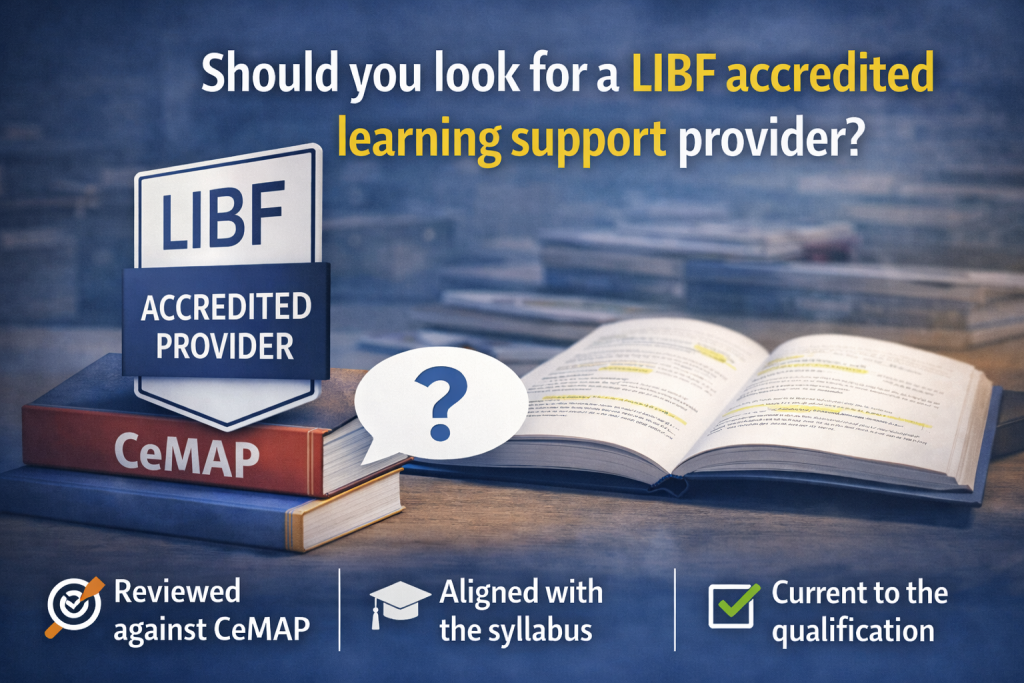

Should you look for a LIBF accredited learning support provider?

Looking for a London Institute of Banking & Finance (LIBF) accredited learning support provider can be one way to assess the quality of study resources.

CeMAP is awarded by LIBF, so accredited providers have had their learning materials reviewed against the qualification standards. This can give learners confidence that the content is aligned with the syllabus.

In practical terms, this may mean:

- Study materials follow the correct CeMAP structure

- Key topics are covered in line with exam requirements

- Content reflects current standards set by LIBF

However, accreditation relates to the quality and relevance of the learning materials, not the level of personal support you will receive.

It does not guarantee:

- Faster completion

- Better exam results

- A specific level of tutor access or feedback

This is why it should be seen as one indicator of effective study support, rather than the only factor.

A balanced approach is to look for:

- Accredited learning materials

- Clear structure and guidance

- Access to tutors when needed

- Opportunities for feedback and exam practice

Together, these give a more complete picture of what your study experience is likely to be.

How does feedback improve your learning?

Feedback is where learning becomes active rather than passive.

Reading materials alone can give a false sense of understanding. You only really test your knowledge when you apply it.

Good CeMAP support includes:

- Practice questions

- Mock exams

- Explanations of correct and incorrect answers

The key part is not just whether an answer is right or wrong, but why.

Effective feedback helps you:

- Spot gaps in your knowledge

- Understand how questions are structured

- Improve exam technique

- Build confidence over time

For example, if you misunderstand a question about mortgage regulation, feedback should explain both the rule and the reasoning behind the correct answer.

Without this, learners may repeat the same mistakes without realising it.

How does study support affect the overall experience?

Study support has a direct impact on how manageable and realistic the qualification feels.

With strong support:

- Learning feels guided rather than overwhelming

- You are less likely to feel stuck

- Progress feels steady and measurable

- Confidence builds gradually

With limited support:

- It can feel unclear whether you are doing things correctly

- Small misunderstandings can build into bigger problems

- Motivation may drop if progress feels uncertain

The difference is not just about passing exams. It is about understanding the material well enough to apply it later in a real role.

This is important because CeMAP is designed to meet the FCA’s education requirements for mortgage advisers. The goal is not just to pass, but to develop a working understanding of how advice and regulation fit together.

What role does flexibility play in good support?

Flexibility is often overlooked, but it is a key part of effective support.

Many people studying CeMAP are:

- Changing careers

- Working full-time

- Managing other commitments

Good support allows you to:

- Study at times that suit you

- Move at your own pace

- Revisit topics when needed

At the same time, flexibility should still be balanced with structure. Too much freedom without guidance can lead to delays or loss of focus.

The best support sits somewhere in the middle. It gives you control over your schedule, while still helping you stay on track.

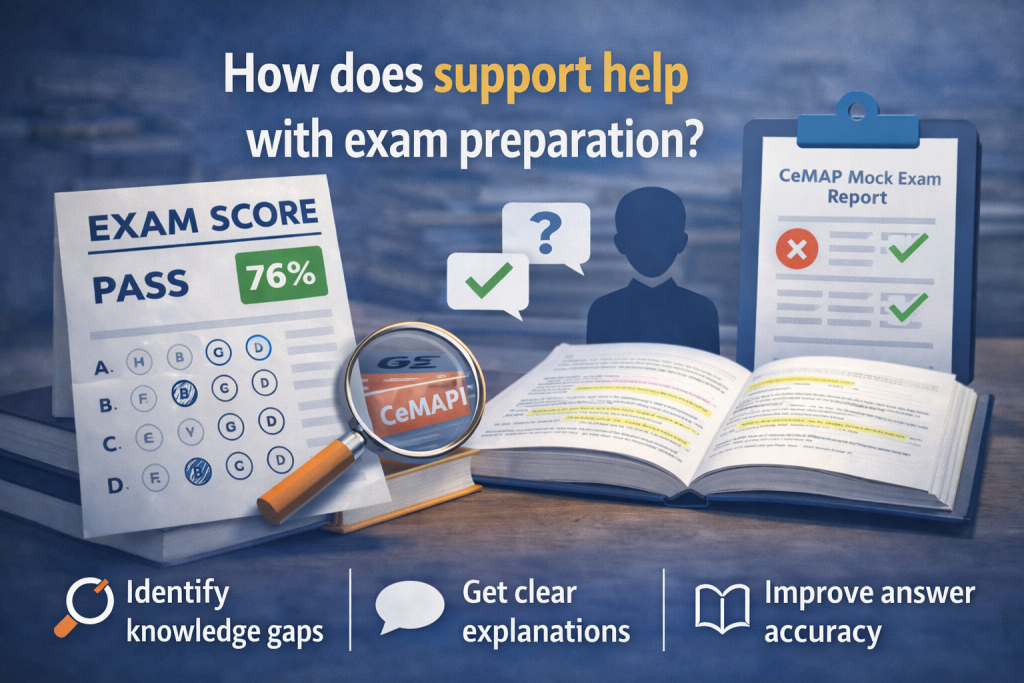

How does support help with exam preparation?

Exam preparation is where support becomes especially valuable.

CeMAP exams are not just about recalling information. They test how well you understand concepts and apply them in realistic scenarios.

Good support in this stage includes:

- Practice exams that reflect real exam style

- Guidance on how questions are worded

- Help with time management during exams

- Techniques for handling more difficult questions

This helps reduce uncertainty.

Rather than going into the exam unsure of what to expect, you have already worked through similar formats and understand how to approach them.

That familiarity can make a noticeable difference in how confident you feel on the day.

What does poor or limited support look like?

Understanding what good support looks like is easier when you recognise the signs of limited support.

This might include:

- No access to tutors or delayed responses

- Large amounts of content with little structure

- Practice questions without clear explanations

- No guidance on exam technique

In these situations, learners often spend more time trying to organise their learning than actually learning.

It does not mean progress is impossible, but it can make the process slower and more frustrating.

Why does study support matter beyond the exams?

CeMAP is the starting point for becoming a mortgage adviser, not the end point.

The way you learn during this stage can affect how prepared you feel when you begin working in the role.

Strong support helps you:

- Understand real-world application, not just theory

- Build confidence in explaining concepts

- Develop habits that carry into professional learning

For example, understanding why certain rules exist makes it easier to apply them when dealing with clients later on.

This is particularly important in a regulated environment, where decisions must be both accurate and justifiable.

Do all learners need the same level of support?

No, and this is where personal preference comes in.

Some learners prefer:

- More independence

- Learning at their own pace with minimal input

Others benefit from:

- Regular guidance

- Clear checkpoints

- Ongoing reassurance that they are progressing correctly

Neither approach is right or wrong.

The key is understanding what helps you stay consistent and confident.

If you are new to financial services, more structured support and tutor access often make the learning curve smoother.

If you already have some background knowledge, you may rely less on support but still benefit from feedback and exam preparation.

How can you tell if support is actually effective?

Effective support is usually noticeable in how you feel while studying.

Signs that support is working well include:

- You understand topics rather than just memorising them

- You know what to study next

- You can identify and correct mistakes

- You feel gradually more confident over time

If you find yourself:

- Re-reading the same material without clarity

- Unsure whether you are progressing correctly

- Avoiding certain topics because they feel confusing

It may be a sign that support is not meeting your needs.

A clear way to think about CeMAP study support

CeMAP study support is best understood as a combination of guidance, structure, and feedback that helps you move from confusion to clarity.

It is not about being constantly assisted. It is about having the right help available at the right time.

At its best, support allows you to:

- Understand what you are learning

- Apply that knowledge in context

- Prepare realistically for exams

- Build confidence step by step

Final thoughts

When asking “What support do you get with CeMAP?”, the more useful question is often:

“What kind of support will help me learn effectively?”

The answer will vary depending on your experience, your schedule, and how you prefer to learn.

What remains consistent is this: good support is practical, structured, and responsive. It helps you understand the material, not just get through it.

And that understanding is what carries forward when you move from studying into real mortgage advice.

Looking for training support?

We offer CeMAP training for learners working towards a career in mortgage advice. Our courses follow the London Institute of Banking & Finance syllabus and are designed to support understanding of mortgage regulation and advice requirements.

Explore our accredited CeMAP training courses

> Futuretrend Financial Training