If you are looking at CeMAP training, one of the most common questions is simple: what am I actually paying for?

A CeMAP course is not just a bundle of revision notes. It is a structured learning experience designed to help you understand the syllabus, apply it, and prepare for assessment in a supported way.

Understanding what is included helps you compare providers properly and avoid choosing based on price alone.

What is included in a CeMAP course?

A CeMAP course usually includes three core elements:

- Teaching or guided learning

- Study materials and resources

- Ongoing learner support

At its most basic, the course is designed to help you move through the CeMAP syllabus in a structured way, rather than trying to work everything out on your own.

CeMAP, awarded by the London Institute of Banking & Finance, is the industry standard qualification for mortgage advisers and meets the education requirements set by the Financial Conduct Authority. Because of that, the syllabus is detailed and quite broad.

A course exists to organise that complexity into something manageable.

What does “teaching” actually mean in a CeMAP course?

Teaching in a CeMAP course can take different forms depending on the provider, but the purpose is the same: to explain the syllabus in a way that builds understanding, not just memorisation.

This might include:

- Tutor-led sessions (online or in person)

- Recorded lessons or walkthroughs

- Topic-by-topic explanations

- Worked examples and discussions

The key difference between teaching and self-study is guidance.

Instead of reading a section and trying to interpret it yourself, the content is explained in a way that highlights what matters, how topics connect, and where learners often struggle.

Good teaching does not just repeat the textbook. It translates it.

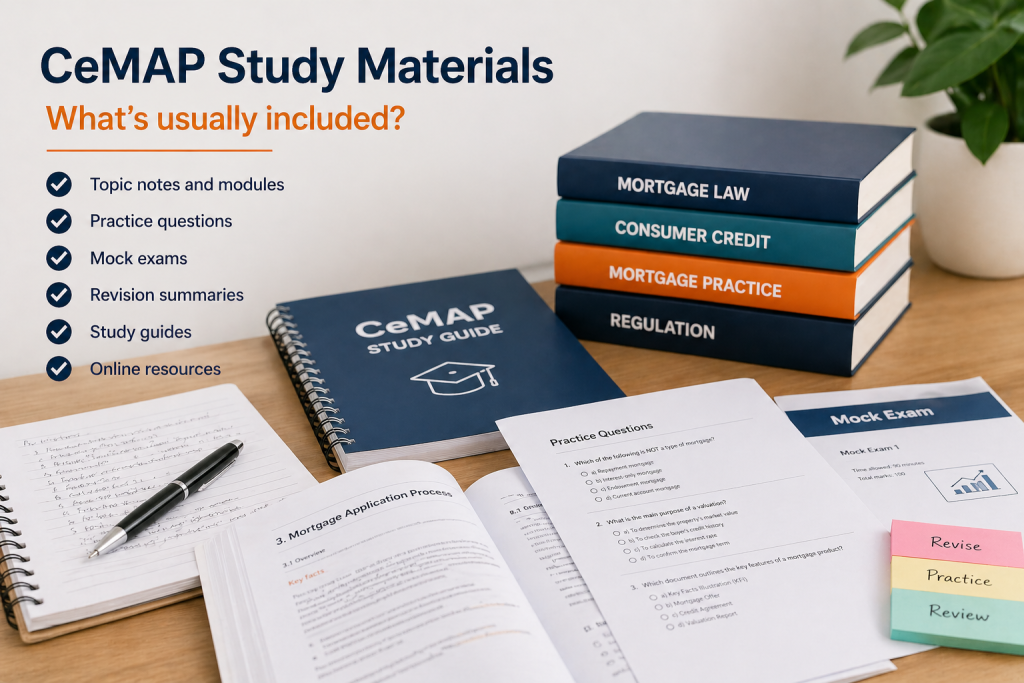

What study materials are usually included?

Most CeMAP courses come with a set of structured study materials designed to support different stages of learning.

These often include:

- Core learning content aligned to the syllabus

- Topic-based notes or modules

- Practice questions or knowledge checks

- Mock exams or assessment-style tests

- Revision summaries

The important point is not just what materials are included, but how they are organised.

A well-structured course breaks the syllabus into manageable sections, often by topic or sub-topic, so you are not faced with everything at once. This makes it easier to track progress and stay consistent.

What is a Study Hub and why does it matter?

Many modern CeMAP providers offer a Study Hub or online learning platform.

This is where the course comes together.

A Study Hub typically includes:

- All learning materials in one place

- Progress tracking

- Structured topic navigation

- Integrated quizzes or tests

- Access to support or tutors

Rather than jumping between PDFs, emails, and notes, everything is centralised.

The value here is structure.

Instead of deciding what to study next, the course guides you through the process step by step. For many learners, this reduces overwhelm and makes it easier to stay on track.

What is the difference between content and guided learning?

This is one of the most important distinctions when comparing CeMAP courses.

Content-only learning means you are given materials and left to work through them yourself.

Guided learning means the course actively helps you understand how to use those materials.

Guided learning often includes:

- Clear study pathways

- Explanations of difficult areas

- Direction on what to focus on

- Reinforcement through questions and feedback

Two courses might both include the same syllabus content, but the experience can feel very different.

Content gives you information.

Guided learning helps you make sense of it.

How important is support in a CeMAP course?

Support is often one of the least visible but most valuable parts of a course.

This can include:

- Access to tutors for questions

- Help with difficult topics

- Clarification on confusing areas

- Guidance when you feel stuck

CeMAP can feel straightforward at first, but some areas require careful understanding. When you hit those points, having support available can make a noticeable difference.

It is not just about getting answers. It is about reducing uncertainty and keeping momentum.

What does structure add that self-study does not?

You can study CeMAP without a course, so it is fair to ask what extra value a structured course provides.

The main difference is organisation and direction.

A structured course:

- Breaks the syllabus into logical sections

- Presents topics in a sensible order

- Reinforces learning as you go

- Helps you avoid missing key areas

Without that structure, learners often:

- Jump between topics

- Spend too long on some areas and not enough on others

- Struggle to judge their progress

- Feel unsure about exam readiness

Structure does not replace effort, but it makes that effort more focused.

Do all CeMAP courses include the same things?

No, and this is where comparisons become important.

Most courses include the core elements, but the depth and quality can vary.

Differences might include:

- Level of tutor involvement

- Quality and clarity of materials

- How detailed the Study Hub is

- Availability of support

- Range of practice questions and mock exams

Two providers might both say they offer “full course materials”, but that could mean very different things in practice.

This is why it is worth looking beyond simple descriptions and understanding what the learning experience actually looks like.

What is an accredited CeMAP learning support provider?

Not all CeMAP training providers are recognised in the same way. Some are listed as accredited learning support providers by the London Institute of Banking & Finance.

An accredited provider has been reviewed by the awarding body and is approved to offer structured learning support for the qualification.

This does not mean the provider delivers the qualification itself. CeMAP is still awarded by the London Institute of Banking & Finance. It means the training provider meets certain standards in how they support learners through the syllabus.

Why does provider approval matter?

Choosing a provider that is approved or accredited adds a layer of reassurance about how the course is structured and delivered.

It suggests that:

- The materials are aligned to the official syllabus

- The course is designed to support understanding, not just content delivery

- The learning experience has been reviewed against recognised standards

That said, accreditation is not a guarantee of outcomes. It does not mean a learner will pass automatically or find the course easy.

What it does offer is confidence that the course has been built with a clear understanding of what the qualification requires.

How does this differ from general training providers?

Some providers offer CeMAP courses without formal accreditation or recognition.

This does not automatically mean the course is poor. However, it does mean:

- The structure and materials have not been reviewed by the awarding body

- The quality can vary more between providers

- You may need to look more closely at what is actually included

In contrast, accredited providers have an additional level of oversight, which can help when comparing options.

What should you look for alongside accreditation?

Accreditation is one factor, but it should not be the only one you rely on.

It is still important to look at:

- How the course is structured

- Whether support is available

- The clarity of the materials

- How the Study Hub or platform works

A strong course combines recognised standards with clear, practical delivery.

How do you know if a course offers real value?

Value in a CeMAP course is not just about how much content is included.

It is about how well that content is delivered and supported.

Signs of a well-developed course include:

- Clear explanations rather than dense text

- Materials broken into manageable topics

- A mix of formats (not just written content)

- Structured progression through the syllabus

- Access to help when needed

Some providers also offer previews, walkthroughs, or sample materials. These can give a clearer idea of what you are actually getting before committing.

Is a CeMAP course just about passing the exam?

A CeMAP course is designed to support exam preparation, but its purpose is broader than that.

The qualification itself is about understanding how mortgage advice works, including regulation, products, and client needs.

A good course helps you:

- Understand concepts, not just memorise facts

- See how topics connect

- Build confidence in applying knowledge

This matters because the exam is testing understanding as well as knowledge.

Simply reading information is not always enough.

Why do some courses feel easier to follow than others?

This usually comes down to how the course is designed, not how “hard” the content is.

Courses that feel easier to follow tend to:

- Use plain, clear explanations

- Avoid unnecessary complexity

- Build topics gradually

- Reinforce learning consistently

Courses that feel difficult often:

- Present too much information at once

- Lack clear structure

- Assume prior knowledge

- Offer limited guidance

The syllabus is the same either way. The difference is how it is delivered.

What should you focus on when comparing CeMAP courses?

When comparing options, it helps to look beyond surface-level features.

Instead of asking “what do I get?”, consider:

- How is the learning structured?

- Is there guidance, or just content?

- What support is available if I struggle?

- How are materials presented and organised?

These questions give a clearer picture of the learning experience.

A simple way to think about it

At its core, a CeMAP course is a combination of:

- Information (the syllabus)

- Explanation (teaching)

- Organisation (structure)

- Reinforcement (practice)

- Support (guidance)

All courses include these in some form, but the balance and quality can vary.

Understanding that helps you make a more informed choice.

A simple way to think about it

A CeMAP course is not just a set of materials. It is a framework for learning a detailed and regulated subject in a manageable way.

The real value comes from how well that framework supports you.

If it provides clear structure, useful explanations, and access to support, it can make the process feel far more straightforward.

If it does not, even good content can feel difficult to use.

That is why understanding what is included matters just as much as deciding to take the qualification in the first place.

Looking for training support?

We offer CeMAP training for learners working towards a career in mortgage advice. Our courses follow the London Institute of Banking & Finance syllabus and are designed to support understanding of mortgage regulation and advice requirements.

Explore our accredited CeMAP training courses

> Futuretrend Financial Training