If you are thinking about becoming a mortgage adviser in the UK, you will quickly come across the term CeMAP. It is not optional, and it is not a company preference. CeMAP exists because mortgage advice is regulated, and advisers must meet a recognised education standard before they can give advice to the public.

This article explains, in simple terms, what CeMAP is, why it exists, who needs it, and what it does and does not allow you to do.

The content follows established UK CeMAP education and quality standards to ensure accuracy and clarity for learners.

What is CeMAP?

CeMAP is the industry-standard qualification for mortgage advisers in the UK.

CeMAP stands for Certificate in Mortgage Advice and Practice. It is awarded by the London Institute of Banking & Finance (LIBF) and is designed to meet the Financial Conduct Authority’s education requirements for mortgage advice.

In simple terms, CeMAP proves that someone understands how mortgages work, how mortgage regulation operates, and how to give suitable advice to clients.

CeMAP is made up of three units that cover:

- The UK financial services environment and regulation

- Mortgage law, products, and repayment methods

- Assessing clients and providing appropriate mortgage advice

A clear definition of CeMAP

CeMAP is a UK mortgage qualification awarded by the London Institute of Banking & Finance that meets the FCA’s educational requirements for giving regulated mortgage advice.

This definition is important because CeMAP is about education. It does not authorise someone to trade, and it does not make them regulated on its own.

Why is CeMAP required for mortgage advice?

Mortgage advice is regulated because it involves large financial commitments and long-term risk for consumers.

Most people borrow significant amounts of money when taking out a mortgage. Poor advice can lead to financial hardship, repossession, or unsuitable long-term commitments. For this reason, mortgage advice in the UK is regulated by the Financial Conduct Authority (FCA).

The FCA does not allow individuals to give mortgage advice unless they meet specific standards. One of those standards is holding an appropriate qualification. CeMAP is the most widely recognised qualification that meets this requirement.

The role of regulation

Regulation exists to:

- Protect consumers from poor or misleading advice

- Ensure advisers understand the rules they must follow

- Create consistent professional standards across the industry

CeMAP supports this by ensuring advisers have a baseline level of technical knowledge and regulatory understanding before they advise clients.

Do you need CeMAP to be a mortgage adviser?

Yes, you need CeMAP, or an equivalent qualification, to give mortgage advice in the UK.

If your role involves recommending mortgage products to clients, you must hold a qualification that meets FCA education standards. CeMAP is the most common qualification used for this purpose.

Without CeMAP (or an accepted equivalent), you cannot legally give regulated mortgage advice, even if you work for an authorised firm.

This applies whether you are:

- Employed by a mortgage brokerage

- Self-employed

- Working under supervision

Training alone is not enough. The qualification itself is required.

Who must hold CeMAP and who does not?

Not everyone working in a mortgage business needs CeMAP. The requirement depends on what you actually do.

Roles that must hold CeMAP

You will need CeMAP if you:

- Give mortgage advice to clients

- Recommend specific mortgage products

- Assess client suitability and affordability as part of advice

These roles are classed as regulated mortgage advice activities.

Roles that do not require CeMAP

You may not need CeMAP if you:

- Carry out purely administrative work

- Collect information without giving advice

- Work in marketing or customer service

- Act as an introducer without recommending products

However, many people in non-advisory roles still choose to study CeMAP because it supports career progression and deeper understanding of the industry.

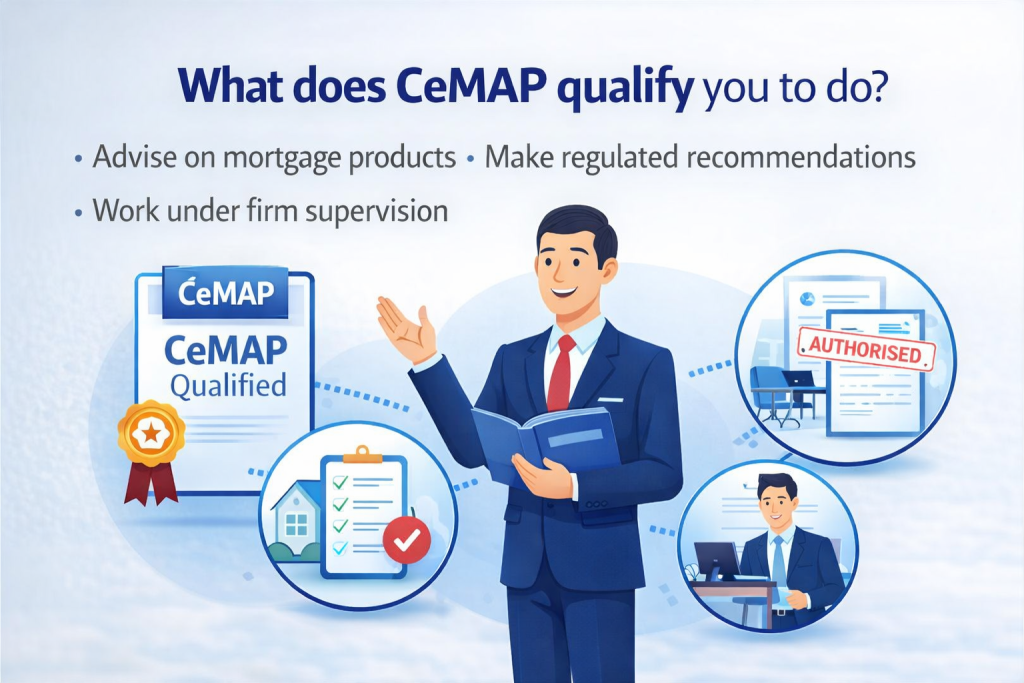

What does CeMAP qualify you to do?

CeMAP qualifies you, from an education perspective, to give mortgage advice once you are working for an authorised firm.

Specifically, CeMAP:

- Meets the FCA’s education requirements for mortgage advisers

- Demonstrates technical and regulatory knowledge

- Allows a firm to consider you for an adviser role

Once you hold CeMAP and are authorised by a firm, you can:

- Advise clients on suitable mortgage products

- Make regulated mortgage recommendations

- Work towards full competent adviser status under supervision

CeMAP is often described as the starting point for a mortgage advice career, not the end point.

What does CeMAP not allow you to do?

CeMAP does not authorise you to trade or operate independently.

This is a common area of confusion, so it is important to be clear.

CeMAP does not:

- Make you FCA authorised

- Allow you to give advice on your own

- Replace firm authorisation

- Remove the need for supervision and competence sign-off

Even with CeMAP, you must work for, or be appointed by, a firm that is authorised by the FCA. The firm is responsible for oversight, compliance, and permissions.

CeMAP is an education requirement. FCA authorisation is a business and regulatory requirement. They are related, but they are not the same thing.

How CeMAP fits into the wider qualification structure

CeMAP is structured as three units, commonly referred to as CeMAP 1, CeMAP 2, and CeMAP 3.

Together, these units build from:

- Understanding regulation and the financial services environment

- Learning how mortgages work in practice

- Applying knowledge to real client scenarios

Many learners study CeMAP in stages, often alongside entry-level roles in mortgage firms. After completing CeMAP, advisers usually move on to supervised practice and, later, more advanced qualifications depending on their career path.

Key points to remember

CeMAP is required because mortgage advice is regulated and consumers need protection.

It is:

- An FCA-recognised education standard

- Awarded by the London Institute of Banking & Finance

- Essential for anyone giving mortgage advice

It is not:

- FCA authorisation

- Permission to advise independently

- A guarantee of employment or success

Understanding this distinction early helps avoid confusion and sets realistic expectations for anyone considering a career in mortgage advice.

Looking for training support?

We offer CeMAP training for learners working towards a career in mortgage advice. Our courses follow the London Institute of Banking & Finance syllabus and are designed to support understanding of mortgage regulation and advice requirements.

Explore our accredited CeMAP training courses

> Futuretrend Financial Training