Mortgage advice is a regulated profession in the UK. Regulation influences almost every part of a mortgage adviser’s role, from the information they gather and the recommendations they make to the records they keep and the training they complete.

For people considering a career in mortgage advice, regulation can sometimes sound complicated or restrictive. In reality, regulation exists to help ensure consumers receive suitable advice, understand the products they are choosing, and are treated fairly throughout the mortgage process.

Understanding how regulation affects mortgage advisers in practice provides a clearer picture of what the role actually involves day to day.

What Is Mortgage Regulation?

Mortgage regulation is the framework of rules and standards that govern how mortgage advice is provided in the UK.

The main regulator is the Financial Conduct Authority (FCA). The FCA sets standards that firms and advisers must follow when advising customers about mortgages and related products.

The purpose of regulation is to create a fair, transparent, and trustworthy mortgage market. It aims to reduce the risk of unsuitable advice, improve consumer understanding, and ensure firms act responsibly.

Mortgage advisers do not simply recommend products based on personal opinion. They work within a regulated environment designed to put customer interests at the centre of the advice process.

Why Does Mortgage Regulation Exist?

Mortgage regulation exists primarily to protect consumers.

For many people, a mortgage is the largest financial commitment they will ever make. Choosing the wrong mortgage could have long-term financial consequences.

Regulation helps ensure that:

- Customers receive clear information

- Advice is based on individual circumstances

- Risks are explained appropriately

- Products are recommended for suitable reasons

- Firms maintain professional standards

- Complaints can be investigated fairly

Without regulation, consumers would have fewer protections and less confidence in the advice they receive.

The regulatory system helps create consistency across the industry while promoting trust between advisers and clients.

How Does Regulation Affect Mortgage Advisers Day to Day?

Regulation affects almost every stage of a mortgage adviser’s work.

Many people imagine advisers spend most of their time comparing mortgage rates. While product knowledge is important, a significant part of the role involves following processes designed to ensure recommendations are appropriate and properly documented.

Day-to-day responsibilities often include:

- Gathering detailed client information

- Understanding customer needs and objectives

- Assessing affordability

- Explaining options clearly

- Documenting recommendations

- Maintaining records

- Completing ongoing training

- Following firm procedures

Regulation shapes how these activities are carried out and helps ensure consistency across the advice process.

Why Do Advisers Need to Gather So Much Information?

One of the most visible effects of regulation is the amount of information advisers must collect from clients.

Before recommending a mortgage, advisers need to understand a customer’s circumstances thoroughly.

This may include:

- Income and employment details

- Existing financial commitments

- Credit history information

- Future plans and objectives

- Deposit availability

- Property details

Some clients are surprised by the number of questions involved. However, these questions are designed to help advisers understand the client’s situation and recommend products that fit their needs.

Without this information, it would be difficult to assess whether a mortgage is suitable.

Gathering detailed information is therefore a core part of regulated mortgage advice rather than an administrative exercise.

How Does Regulation Influence Mortgage Recommendations?

Regulation requires advisers to have clear reasons for the recommendations they make.

A mortgage recommendation should be based on the customer’s circumstances rather than personal preference or convenience.

When assessing options, advisers may consider factors such as:

- Affordability

- Interest rate structure

- Product flexibility

- Fees and charges

- Mortgage term

- Customer objectives

The goal is to identify products that meet the client’s needs while ensuring they understand how the mortgage works.

Regulation encourages advisers to focus on suitability rather than simply finding the lowest interest rate available.

A mortgage with a lower rate is not always the most appropriate solution if other features better match the client’s circumstances.

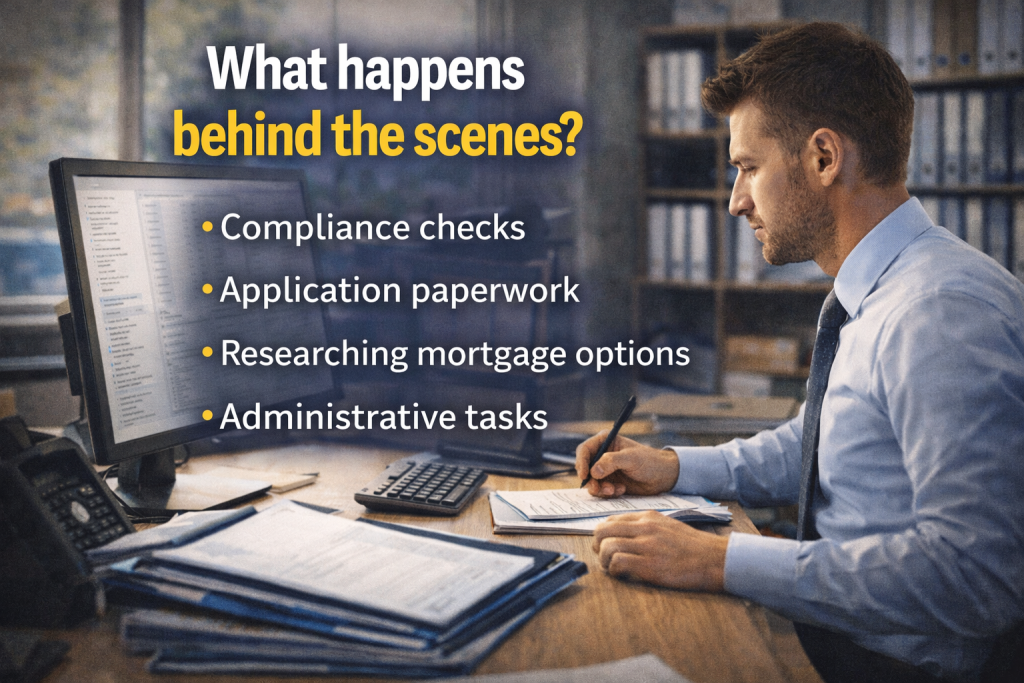

Why Is Record Keeping So Important?

Record keeping is a major part of working in a regulated profession.

Mortgage advisers are expected to maintain accurate records of:

- Customer discussions

- Information gathered

- Recommendations provided

- Supporting evidence

- Key decisions made during the advice process

Good record keeping helps demonstrate why a recommendation was made and what information was considered at the time.

It also helps protect both customers and advisers if questions arise later about the advice provided.

Many people outside the industry underestimate how much documentation forms part of the adviser role.

While clients often see the meetings and recommendations, there is usually significant work taking place behind the scenes.

How Does Regulation Support Consumer Protection?

Consumer protection sits at the heart of mortgage regulation.

The regulatory framework aims to ensure customers are treated fairly throughout the mortgage process.

This includes helping consumers:

- Understand products clearly

- Make informed decisions

- Receive appropriate recommendations

- Access complaint procedures if needed

- Understand costs and commitments

Mortgage advisers play an important role in delivering these protections.

Rather than simply arranging mortgages, advisers help customers understand important information and make decisions based on their circumstances.

This consumer-focused approach is one reason mortgage advice remains a regulated activity.

Does Regulation Affect How Advisers Communicate With Clients?

Yes. Regulation influences how advisers communicate with customers.

Information should be presented clearly and fairly. Advisers must avoid creating misunderstandings or giving incomplete explanations.

In practice, this means advisers often spend time discussing:

- Product features

- Risks and limitations

- Costs and fees

- Repayment obligations

- Potential future changes

Good communication is an essential skill for mortgage advisers.

Regulation supports transparency by encouraging advisers to ensure customers understand the information they are receiving before making decisions.

What Ongoing Responsibilities Do Mortgage Advisers Have?

Regulation does not end once an adviser becomes qualified.

Mortgage advisers are expected to maintain professional standards throughout their careers.

Ongoing responsibilities may include:

- Continuing professional development (CPD)

- Keeping up with regulatory changes

- Maintaining product knowledge

- Following firm compliance procedures

- Completing internal training

- Demonstrating competence in their role

The mortgage market changes over time, and advisers are expected to keep their knowledge current.

This commitment to ongoing learning helps ensure consumers continue to receive informed and accurate advice.

Does Regulation Make Mortgage Advice More Difficult?

Regulation can make the advice process more detailed, but its purpose is not to make life difficult for advisers or customers.

The additional processes are designed to support good decision-making and consumer protection.

Many advisers view regulation as a framework that helps maintain professional standards across the industry.

While compliance responsibilities form part of the role, they also contribute to the trust that consumers place in regulated mortgage advice.

For people considering a career in the sector, understanding and following regulatory requirements becomes a normal part of everyday working life.

How Does Regulation Affect Mortgage Advisers?

Mortgage regulation affects mortgage advisers by shaping how they gather information, assess customer needs, make recommendations, communicate with clients, maintain records, and develop their professional knowledge.

The regulatory framework exists to protect consumers and promote fair outcomes. Rather than being separate from the adviser role, regulation is woven into the daily activities that advisers carry out.

For aspiring advisers studying towards qualifications such as CeMAP, understanding regulation is an important part of understanding the profession itself. Mortgage advice is not simply about finding products. It is about helping customers make informed decisions within a structured and regulated environment that prioritises consumer protection, suitability, and professional responsibility.

Final Thoughts

Mortgage regulation is often viewed as a set of rules advisers must follow, but in practice it shapes how professional mortgage advice is delivered every day.

From gathering client information and assessing affordability to explaining recommendations and maintaining records, regulation influences the entire advice process. Its purpose is to help ensure consumers receive suitable advice, understand their options, and are treated fairly throughout their mortgage journey.

For those considering a career as a mortgage adviser, understanding regulation is an important part of understanding the profession itself. Successful advisers do more than compare mortgage products. They combine technical knowledge, communication skills, and professional responsibility to help clients make informed decisions within a regulated framework.

While regulation creates additional responsibilities, it also helps build trust in the advice process, benefiting both advisers and the customers they serve.

This works well because it summarises the key themes of consumer protection, professionalism, trust, and day-to-day impact without repeating the article word for word, while also giving AI Overviews and search engines a strong concluding summary.

Looking for training support?

We offer CeMAP training for learners working towards a career in mortgage advice. Our courses follow the London Institute of Banking & Finance syllabus and are designed to support understanding of mortgage regulation and advice requirements.

Explore our accredited CeMAP training courses

> Futuretrend Financial Training