Completing CeMAP is a major step towards becoming a mortgage adviser. It shows that you understand the rules, products, and responsibilities involved in giving mortgage advice in the UK.

However, finishing CeMAP does not mean you can immediately start advising clients. There are still important steps between passing the exams and working in a regulated role.

This guide explains what happens next, what your options are, and what you should realistically expect.

What can you do after CeMAP?

After completing CeMAP, you can begin working towards a role in mortgage advice, but you cannot give regulated advice independently straight away.

In simple terms:

- CeMAP proves your knowledge

- Authorisation allows you to advise

- Experience and supervision bridge the gap between the two

Most learners move into entry-level roles within mortgage or financial services and then progress under supervision until they are fully authorised.

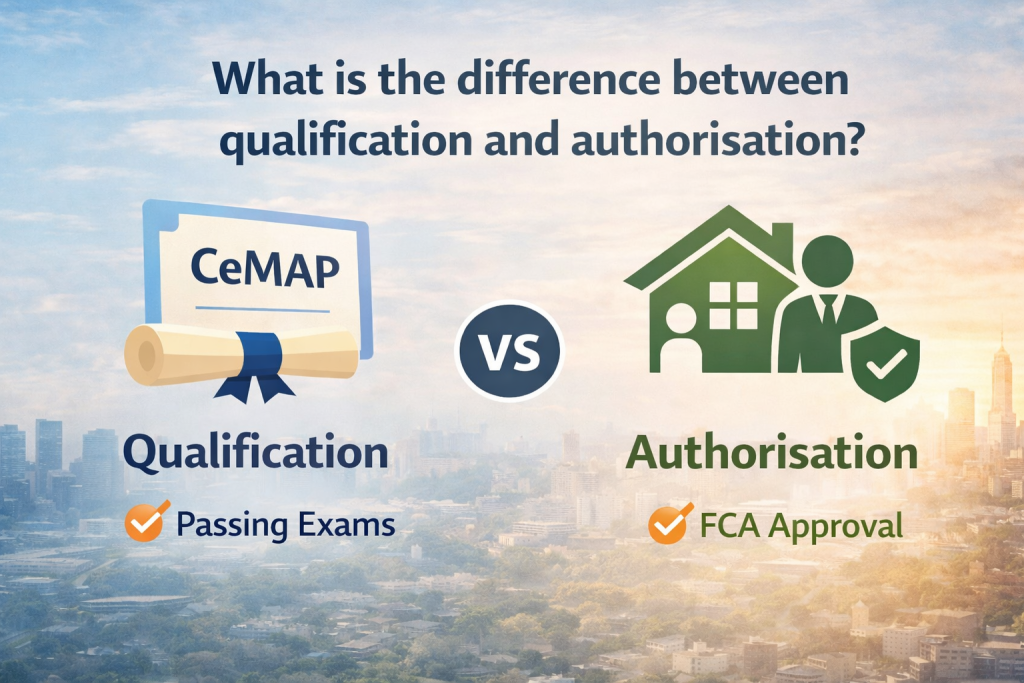

Does passing CeMAP mean you are qualified to give advice?

No. Passing CeMAP means you meet the education requirement, not the authorisation requirement.

CeMAP is awarded by the London Institute of Banking & Finance and meets the standards set by the Financial Conduct Authority for mortgage advisers.

A clear way to understand it:

- CeMAP = knowledge and exam success

- Authorisation = permission to advise clients

To give regulated mortgage advice, you must be:

- Authorised by the FCA directly, or

- Working under a firm that is authorised by the FCA

This is a key distinction that often catches learners out.

What is the difference between qualification and authorisation?

The difference comes down to responsibility and regulation.

Qualification (CeMAP):

- Confirms you understand mortgage regulation, products, and advice principles

- Shows you have passed structured exams

- Is required before entering an advisory role

Authorisation (FCA):

- Allows you to give regulated advice to clients

- Requires you to work within a regulated firm

- Involves oversight, monitoring, and compliance checks

Most new advisers do not apply for direct FCA authorisation themselves. Instead, they join a firm and become an appointed representative or employee working under that firm’s permissions.

What are the most common next steps after CeMAP?

There is no single path, but most learners follow a similar progression.

1. Apply for entry-level roles

Common starting roles include:

- Trainee mortgage adviser

- Mortgage administrator

- Paraplanner or case handler

- Customer support roles in financial services

These roles help you understand how mortgage cases work in practice, not just in theory.

Some learners move straight into trainee adviser roles, while others build experience in support positions first.

2. Join a regulated firm

To move towards advising, you need to work within an FCA-authorised environment.

This could be:

- A mortgage brokerage

- A bank or building society

- A financial advice firm

The firm becomes responsible for supervising your work and ensuring you meet regulatory standards.

3. Begin supervised advising

Before advising independently, you will usually work under supervision.

This means:

- Your advice is checked before being finalised

- You follow structured processes and compliance rules

- You build confidence with real client scenarios

This stage is often referred to as being “competent under supervision”.

What does supervision look like in practice?

Supervision is a core part of becoming a mortgage adviser.

It is not just a formality. It is how firms ensure that advice is accurate, suitable, and compliant.

During supervision, you may:

- Sit in on client meetings

- Handle parts of the advice process

- Have your recommendations reviewed

- Receive feedback on your decisions

Your progress is usually tracked through a competency framework, which assesses whether you can:

- Gather accurate client information

- Recommend suitable mortgage products

- Follow regulatory requirements

- Communicate clearly with clients

Only when you meet these standards can you move towards independent advising.

How long does it take to become a fully authorised adviser?

There is no fixed timeline.

It depends on:

- The firm you join

- The level of support and training provided

- Your own pace of learning and confidence

Some learners progress within a few months, while others take longer to build experience.

It is better to focus on becoming competent and confident rather than rushing the process.

Do you need additional qualifications after CeMAP?

CeMAP is the main qualification required to start giving mortgage advice, but learning does not stop there.

In practice, you will continue developing your knowledge in areas such as:

- Protection products (life insurance, income protection)

- Specialist lending (buy-to-let, adverse credit)

- Changing regulations and market conditions

Some advisers choose to take further qualifications, but this is not always required early in your career.

What ongoing learning is expected?

Mortgage advice is a regulated profession, which means ongoing learning is essential.

Most advisers are required to complete:

- Continuing Professional Development (CPD)

- Regular compliance training

- Updates on regulatory changes

This ensures that advice remains accurate and up to date.

The industry does not stand still. Rules change, products evolve, and client needs shift over time.

Can you work in financial services without becoming an adviser?

Yes, and many people do.

After CeMAP, you are not limited to advisory roles. Some learners choose to stay in support or operational positions.

Examples include:

- Mortgage processing and administration

- Compliance and quality assurance

- Client relationship management

- Business development roles

These roles still benefit from CeMAP knowledge and can offer stable career paths without the responsibility of giving advice.

What challenges do learners face after CeMAP?

Finishing the exams is a big achievement, but the transition into work can feel uncertain.

Common challenges include:

Understanding the job market

Some learners expect immediate adviser roles, but many positions require practical experience or start at trainee level.

Adjusting from theory to practice

CeMAP teaches principles, but real cases involve:

- Complex client situations

- Changing lender criteria

- Time pressures and deadlines

Building confidence

Even with strong exam results, applying knowledge in real scenarios can take time.

This is normal and expected.

What support should you look for from an employer?

Not all roles offer the same level of support, and this can make a big difference early in your career.

Helpful support structures include:

- Clear training pathways

- Access to experienced advisers

- Regular feedback and mentoring

- Structured supervision

A role that offers guidance and development is often more valuable than one that expects immediate performance.

Is there a “best” route after CeMAP?

No, and it is worth being cautious of anyone suggesting there is.

Your path depends on:

- Your previous experience

- Your confidence level

- The type of work environment you prefer

Some people thrive in fast-paced advisory roles straight away. Others benefit from starting in support roles and building gradually.

Both approaches can lead to the same outcome.

What should you focus on after passing CeMAP?

Rather than worrying about the “perfect” next step, it helps to focus on a few practical priorities:

1. Gaining real-world experience

Understanding how mortgage cases work day to day is essential.

2. Learning from others

Experienced advisers can offer insights that exams cannot.

3. Developing communication skills

Advising is not just about knowledge. It is about explaining options clearly to clients.

4. Staying patient

Progression takes time, and rushing can lead to mistakes.

Final thoughts

Completing CeMAP is the start of your mortgage career, not the finish line.

It shows that you have the knowledge required to enter the profession, but becoming a mortgage adviser involves:

- Working within a regulated environment

- Gaining practical experience

- Developing confidence under supervision

- Continuing to learn over time

If you keep your expectations realistic and focus on steady progress, CeMAP can open the door to a structured and professional career in financial services.

Looking for training support?

We offer CeMAP training for learners working towards a career in mortgage advice. Our courses follow the London Institute of Banking & Finance syllabus and are designed to support understanding of mortgage regulation and advice requirements.

Explore our accredited CeMAP training courses

> Futuretrend Financial Training