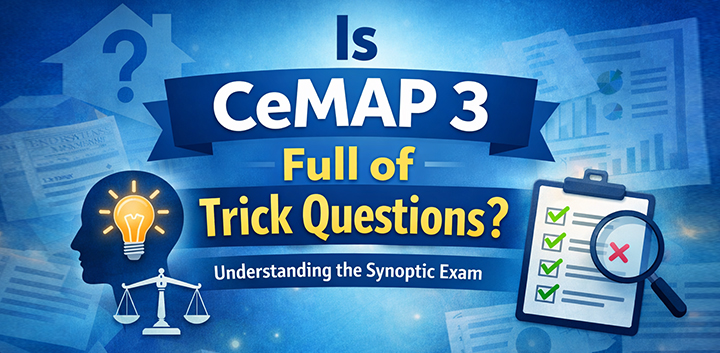

Many learners approaching CeMAP 3 ask the same thing:

“Is CeMAP 3 full of trick questions?”

The short answer is no.

CeMAP 3 is not designed to trick you. It is designed to assess judgement.

Understanding that distinction changes how the synoptic module feels. It shifts the focus away from hunting for traps and towards understanding what the assessment is really measuring.

What Is CeMAP 3 and What Is It Designed to Test?

CeMAP 3 is the final module of the Certificate in Mortgage Advice and Practice, awarded by the London Institute of Banking & Finance.

It is a synoptic assessment, meaning it brings together knowledge from earlier modules and tests how well you can apply it.

CeMAP as a qualification meets the education requirements set by the Financial Conduct Authority for those who wish to give mortgage advice in the UK. However, meeting education requirements is not the same as memorising rules. Advisers must demonstrate the ability to make appropriate, suitable recommendations.

CeMAP 3 exists to assess that ability.

It does not test whether you can recall isolated facts.

It tests whether you can use knowledge responsibly.

Is CeMAP 3 Full of Trick Questions?

No. CeMAP 3 is not written to mislead candidates.

What sometimes feels like a trick question is usually a question that requires:

- Careful reading

- Balanced thinking

- An understanding of suitability

- The ability to distinguish between “possible” and “appropriate”

When learners expect factual recall and instead face judgement-based scenarios, it can feel uncomfortable. That discomfort is often mistaken for trickery.

But the assessment is not trying to catch you out. It is checking whether you can think like a mortgage adviser.

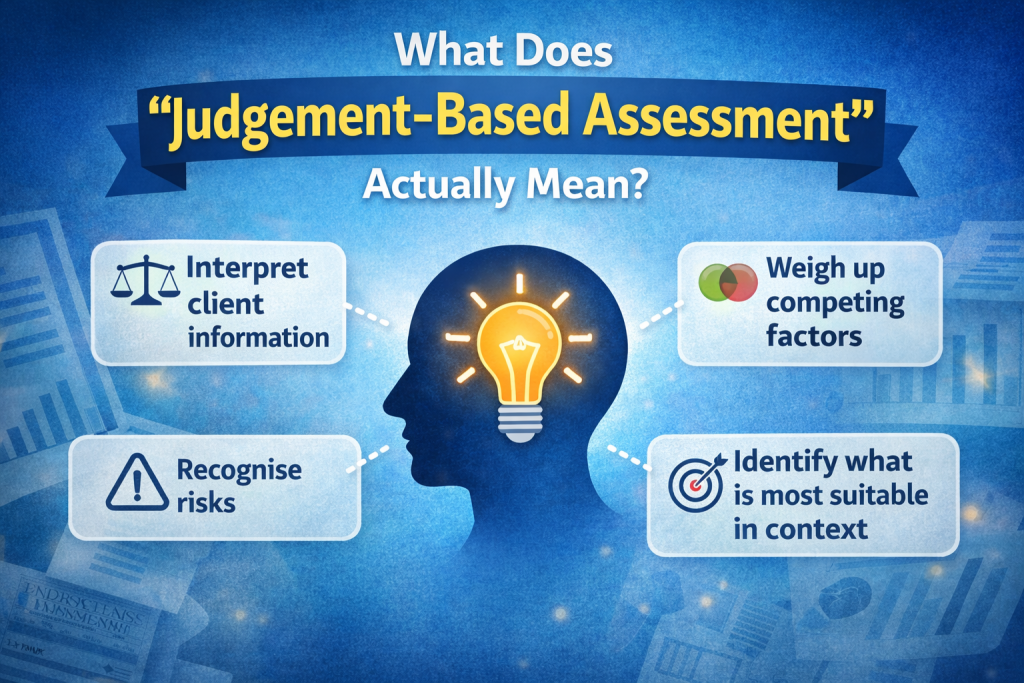

What Does “Judgement-Based Assessment” Actually Mean?

A judgement-based assessment tests your ability to:

- Interpret client information

- Weigh up competing factors

- Recognise risks

- Identify what is most suitable in context

In real life, mortgage advice is rarely about one clear rule. Two products may technically fit a client’s circumstances. One may be more suitable based on risk tolerance, long-term plans, income stability, or regulatory considerations.

CeMAP 3 reflects that reality.

Judgement-based assessment means:

You are being tested on decision quality, not memory.

This is very different from modules that focus more heavily on definitions, regulation, or standalone knowledge areas.

Why Does CeMAP 3 Feel Harder Than Earlier Modules?

Some learners find CeMAP 3 more demanding because it changes the type of thinking required.

Earlier modules such as Financial Services Regulation and Ethics focus more clearly on defined rules, frameworks and principles. There is often a right answer based on regulation.

CeMAP 3 moves into applied suitability.

Instead of asking:

What is the rule?

It is effectively asking:

What would be the most appropriate course of action for this client?

That shift can feel unsettling. There is often more than one answer that looks reasonable at first glance. The task is to identify the most suitable option based on the client’s full circumstances.

That is not a trick. It is professional judgement.

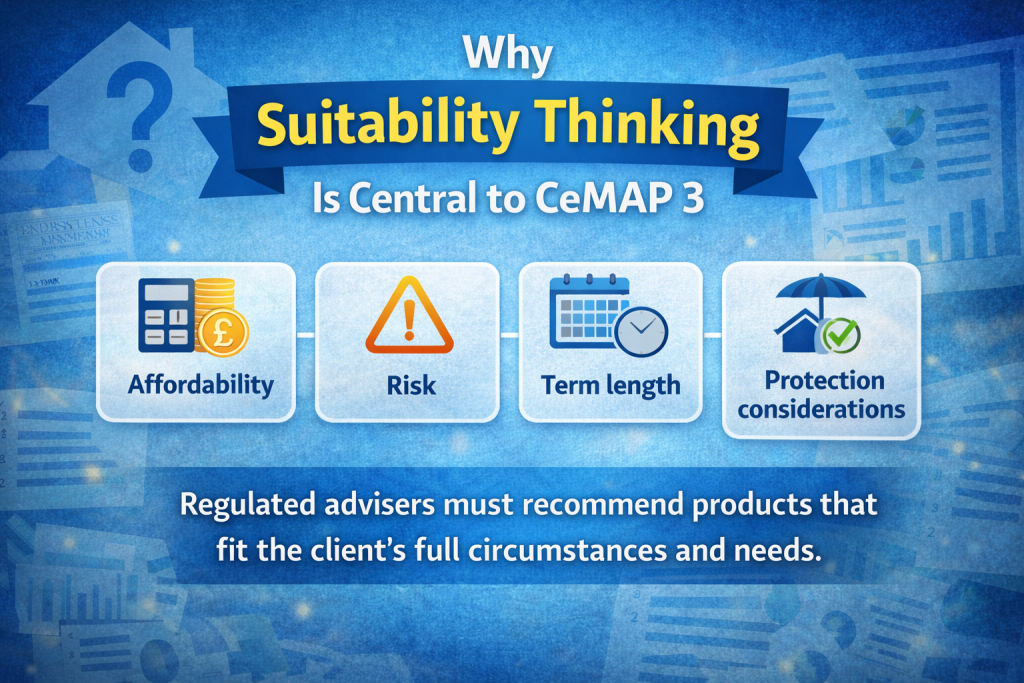

Why Suitability Thinking Is Central to CeMAP 3

Suitability is the foundation of regulated mortgage advice.

A mortgage adviser must recommend products that are appropriate for the client’s needs, objectives and financial situation. This includes:

- Affordability

- Risk

- Term length

- Repayment method

- Future plans

- Protection considerations

CeMAP 3 assesses whether you understand how these pieces fit together.

It is not enough to know what an interest-only mortgage is. You must recognise when it may or may not be suitable.

It is not enough to know what a fixed rate does. You must consider whether stability or flexibility better matches a client’s situation.

That is the essence of judgement.

Why Learners Sometimes Assume There Are Trick Questions

There are a few common reasons why the “trick question” myth persists.

1. Confidence drops when answers are less obvious

In knowledge-based modules, you may feel more certain. You either know the rule or you do not.

In CeMAP 3, two options can appear plausible. Choosing between them requires deeper evaluation. That uncertainty can feel like a trap, even when it is not.

2. Over-reliance on memorisation

If preparation has focused heavily on memorising facts without understanding how they interact, the synoptic paper can feel unfamiliar.

CeMAP 3 rewards understanding. Pure recall is rarely enough.

3. Expecting hidden wording tricks

Some candidates assume questions are deliberately written to mislead. In reality, professional exam bodies design assessments to be fair, consistent and aligned to learning outcomes.

The aim is to measure competence, not to reduce pass rates.

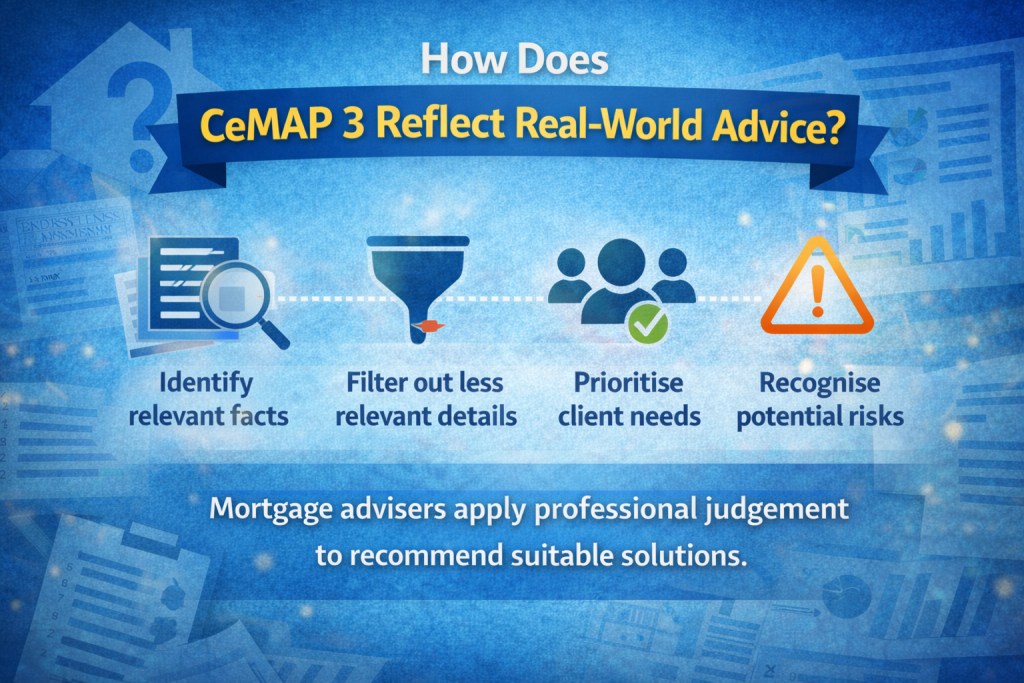

How Does CeMAP 3 Reflect Real-World Advice?

Mortgage advice is not theoretical.

Advisers gather information, assess risk, consider lender criteria, and recommend solutions that are in the client’s best interests.

Real clients do not present in neat textbook scenarios. They have mixed priorities, imperfect finances and changing plans.

CeMAP 3 mirrors that environment in a structured way.

It tests whether you can:

- Identify relevant facts

- Filter out less relevant details

- Prioritise client needs

- Recognise potential risks

- Apply regulatory principles

This is not about spotting tricks. It is about showing that you can think responsibly.

Does CeMAP 3 Try to Catch You Out?

No. Professional awarding bodies design synoptic assessments to ensure consistency and fairness.

The purpose of CeMAP 3 is to confirm that a candidate:

- Understands core mortgage knowledge

- Can apply that knowledge appropriately

- Can recognise suitable and unsuitable recommendations

- Understands ethical responsibility

If a question feels difficult, it is usually because it requires careful evaluation of all the information provided.

Difficulty does not equal deception.

Why Judgement Matters More Than Perfect Recall

In regulated financial services, correct judgement protects:

- The client

- The firm

- The adviser

Regulation exists to ensure consumers receive appropriate advice. The Financial Conduct Authority sets standards to ensure fair treatment of customers. Education standards, including CeMAP, exist to support that framework.

A qualification that only tested memory would not be enough.

CeMAP 3 therefore assesses whether you can:

- Balance competing priorities

- Recognise unsuitable risks

- Understand long-term consequences

- Apply ethical principles

That is why the exam focuses on judgement.

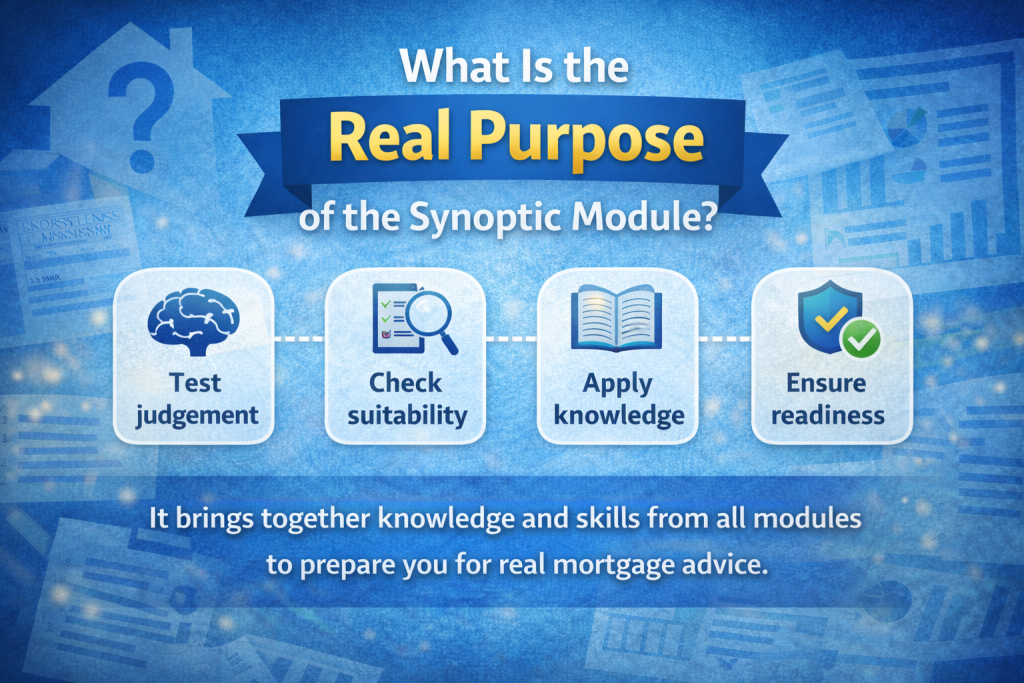

What Is the Real Purpose of the Synoptic Module?

The word “synoptic” simply means it draws together knowledge from across the qualification.

CeMAP 3 is not a new subject. It is the integration of everything learned earlier.

Its purpose is to confirm that you can:

- Combine regulatory understanding

- Apply product knowledge

- Interpret client information

- Make appropriate decisions

It is a bridge between theory and professional practice.

Should You Be Worried About Hidden Tricks?

There is no evidence that CeMAP 3 is designed around hidden traps or deceptive wording.

What it does require is:

- Careful reading

- Structured thinking

- Calm evaluation

If something feels like a trick, pause and ask:

Is this testing my knowledge of a rule, or my judgement about suitability?

Most often, it is the latter.

Understanding that reduces anxiety.

A Clear Answer: Is CeMAP 3 Full of Trick Questions?

No.

CeMAP 3 is not built around trick questions. It is built around professional judgement.

It assesses your ability to think like a mortgage adviser. It checks whether you can apply knowledge responsibly, ethically and appropriately.

When learners reframe the exam as a judgement assessment rather than a memory test, it becomes clearer why the questions are structured the way they are.

Final Thoughts: Reframing How You View CeMAP 3

CeMAP 3 often feels different because it asks you to think differently.

It moves from:

“What is the correct definition?”

to

“What is the most suitable outcome for this client?”

That shift is deliberate.

The mortgage advice profession relies on good judgement. The synoptic module exists to reflect that responsibility.

If you approach CeMAP 3 expecting tricks, you may see complexity as deception.

If you approach it expecting judgement, the structure begins to make sense.

CeMAP 3 is not trying to catch you out.

It is asking whether you are ready to think like an adviser.

Looking for training support?

We offer CeMAP training for learners working towards a career in mortgage advice. Our courses follow the London Institute of Banking & Finance syllabus and are designed to support understanding of mortgage regulation and advice requirements.

Explore our accredited CeMAP training courses

> Futuretrend Financial Training