Many learners ask a simple question before they begin: how hard is CeMAP?

Many learners ask a simple question before they begin: how hard is CeMAP?

The honest answer is that the CeMAP exams are academically manageable for most people, but they require structured preparation and consistent study. They are not designed to catch people out, yet they do test detailed knowledge, regulation, ethics, and the ability to apply what you have learned. For some, the exams feel straightforward. For others, they feel demanding. The difference usually comes down to preparation, familiarity with financial concepts, and confidence with multiple-choice exams.

CeMAP is the industry standard qualification for mortgage advisers in the UK. It is awarded by the London Institute of Banking & Finance and meets the Financial Conduct Authority’s education requirements for giving mortgage advice. Because it leads to a regulated profession, the exams must test knowledge and ethical understanding properly. That is why they feel serious.

This article explains why difficulty is subjective, how the modules differ under the current syllabus, and why preparation matters more than natural ability.

Why Does CeMAP Feel Hard for Some People?

CeMAP often feels hard because it combines new terminology, regulation, ethics, and exam pressure.

For learners who have never worked in financial services, terms relating to regulatory frameworks, conduct rules, and ethical responsibilities can feel unfamiliar. Even core mortgage concepts such as loan-to-value ratios or different repayment structures may be new. That initial learning curve can create the impression that the qualification is harder than it actually is.

Does Previous Experience Make a Difference?

Yes, but not always in the way people expect.

Someone with experience in banking or estate agency may recognise certain mortgage concepts. That familiarity can reduce learning time in CeMAP 2. However, regulatory and ethical content in CeMAP 1 still needs to be learned carefully, regardless of background.

Learners from unrelated careers often succeed because they approach the material methodically. CeMAP does not require advanced mathematics or essay writing. It requires understanding and careful recall.

Is It an Academic Exam?

CeMAP is knowledge-based rather than essay-based. You are tested through multiple-choice questions and, in the final module, case-study style assessment. You are not required to write long answers. Instead, you must recognise the correct response from several options.

For many people, this format feels manageable. For others, multiple-choice exams create uncertainty because more than one answer can appear reasonable. That is where careful reading becomes essential.

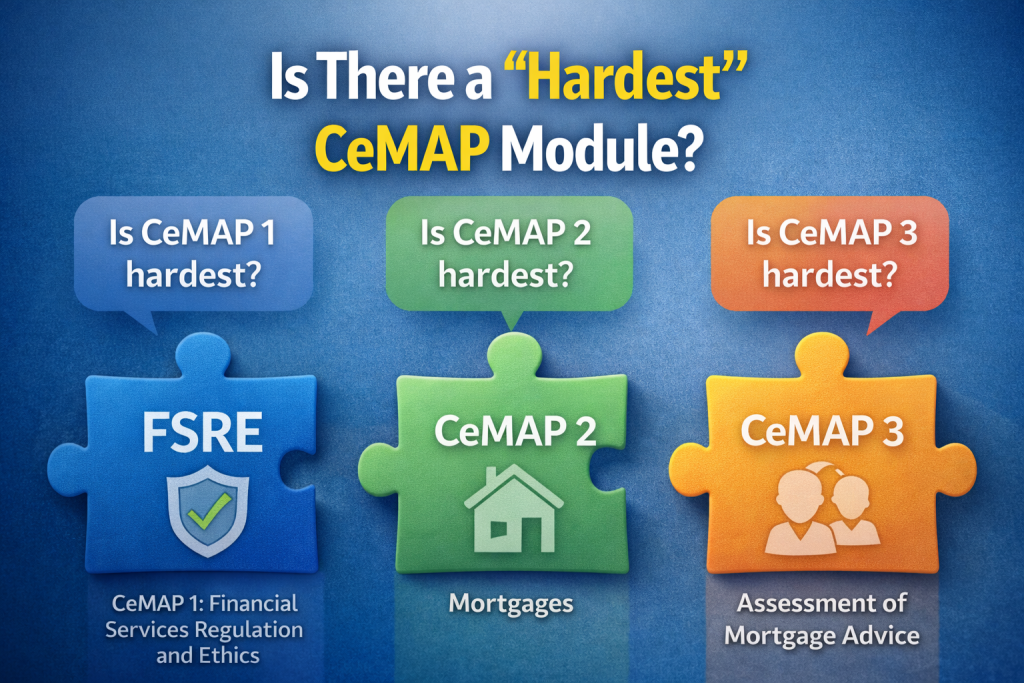

What Makes One Module Feel Harder Than Another?

CeMAP is structured in three modules. Each feels challenging for different reasons.

The modules are designed to build on each other. They do not test identical skills, so difficulty can feel different at each stage.

Under the updated 2025/26 syllabus, the modules are:

CeMAP 1: Financial Services Regulation and Ethics (FSRE)

CeMAP 2: Mortgages

CeMAP 3: Assessment of Mortgage Advice

The content focus has shifted slightly in CeMAP 1, and that affects how learners experience the difficulty.

CeMAP 1: Financial Services Regulation and Ethics (FSRE)

CeMAP 1 focuses on financial services regulation and ethical standards.

It covers the UK regulatory framework, the role of the Financial Conduct Authority, principles of conduct, consumer protection, and ethical responsibilities within financial services. Mortgage knowledge is still included, but the emphasis is on regulation and professional standards.

Many learners find this module challenging because of the volume of detailed definitions and the precision required in understanding regulatory language. The difficulty lies in accuracy rather than complexity.

For those new to financial services, this can feel abstract at first. Once the structure of regulation and ethical principles becomes clear, it tends to feel more logical.

CeMAP 2: Mortgages

CeMAP 2 concentrates on mortgage products and how they operate in practice.

This includes repayment methods, interest types, property considerations, underwriting factors, and different lending scenarios. The subject matter is more product-focused and practical.

Learners who prefer tangible examples sometimes find this module easier because they can visualise how mortgages work. Others find it demanding because of the range of product knowledge required.

The challenge is applying knowledge accurately rather than memorising rules alone.

CeMAP 3: Assessment of Mortgage Advice

CeMAP 3 assesses your ability to apply knowledge in realistic client situations.

It uses case-study style questions to test whether you can identify suitable advice within regulatory and ethical boundaries. It draws directly from content covered in both CeMAP 1 and CeMAP 2.

Some learners find this the hardest module because it requires judgement and careful interpretation of client information. Others find it more intuitive because it mirrors real mortgage advice scenarios.

The perception depends on whether you feel more comfortable recalling structured rules or applying them in context.

Is There a “Hardest” CeMAP Module?

There is no single hardest CeMAP module for everyone.

Some learners say CeMAP 1 feels hardest because of the regulatory and ethical detail. Others say CeMAP 3 feels hardest because of the case-study format. The perception usually reflects personal strengths and learning style.

If you prefer structured theory and definitions, CeMAP 1 may feel manageable.

If you prefer product knowledge, CeMAP 2 may feel more straightforward.

If you prefer applied scenarios, CeMAP 3 may feel more natural.

The qualification is designed to test competence across regulation, ethics, product knowledge, and advice skills. It is not structured so that one module is deliberately more difficult than another.

How Hard Is CeMAP Compared to Other Qualifications?

CeMAP sits at Level 3 on the Regulated Qualifications Framework. This is broadly comparable to A-level standard in terms of academic level.

Most learners taking CeMAP are adults balancing work and other commitments. Time management and consistent study usually matter more than academic background.

CeMAP does not require advanced mathematics. Calculations are limited and practical. The main requirement is understanding regulation, ethics, and mortgage structures clearly.

Does the Pass Mark Mean It Is Difficult?

The pass mark reflects the standard required to meet regulatory expectations, not an attempt to make the exam difficult.

Because mortgage advice is a regulated activity, the Financial Conduct Authority expects advisers to demonstrate knowledge and ethical awareness before giving advice to clients. The exams are structured to confirm that standard.

They are not designed to reduce pass numbers. They are designed to confirm competence.

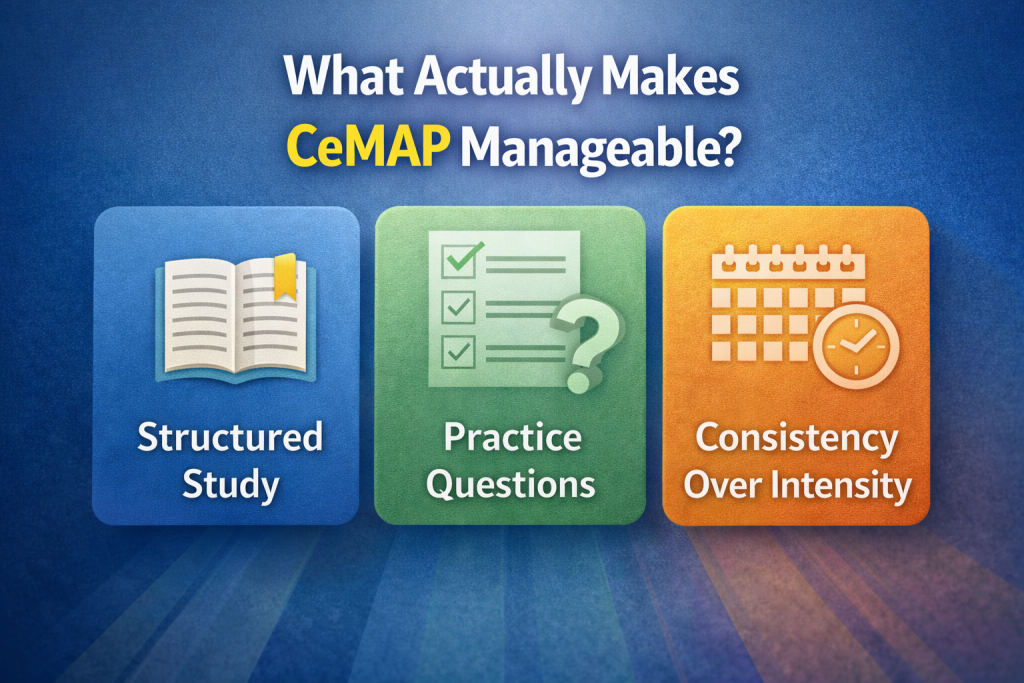

What Actually Makes CeMAP Manageable?

Preparation makes CeMAP manageable.

Most learners who initially feel that CeMAP is hard change their view once they understand the structure and style of questioning.

Structured Study

Breaking the syllabus into manageable sections prevents overwhelm. CeMAP content can appear large when viewed as a whole. Studied in stages, it becomes clearer.

Practice Questions

Becoming comfortable with multiple-choice questions changes how difficult the exam feels. Practice helps you recognise how questions are framed and how distractor answers are constructed.

Consistency Over Intensity

Short, regular study sessions are often more effective than occasional long sessions. The knowledge builds logically across the three modules.

Does Intelligence Determine Success in CeMAP?

CeMAP does not require exceptional academic ability.

Success is usually linked to preparation, organisation, and attention to detail. Learners from a wide range of educational backgrounds complete the qualification each year.

The exams test understanding of regulation, ethics, and mortgage practice. Being methodical often matters more than being naturally academic.

Why Do Some Learners Feel Overwhelmed at the Start?

CeMAP introduces a regulated and ethically structured environment with precise terminology. That can feel unfamiliar.

Regulation and ethics require careful wording. Small differences in phrasing can change meaning. This can create early frustration, particularly in CeMAP 1.

Once learners adjust to that precision, confidence usually improves. What feels complex at first often becomes routine with repetition.

Is Exam Anxiety Making CeMAP Feel Harder?

In many cases, yes.

Anxiety can amplify perceived difficulty. Learners may know the content but doubt themselves during the exam. Multiple-choice formats can increase second-guessing.

Clear preparation and familiarity with the structure reduce this effect.

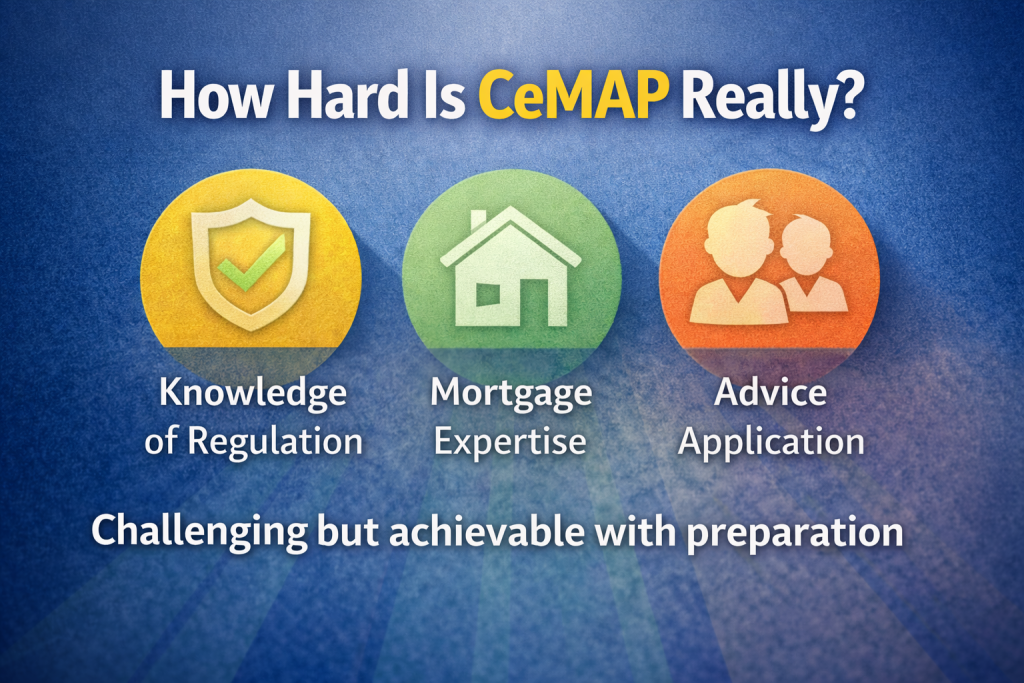

How Hard Is CeMAP Really?

CeMAP is challenging but achievable.

It is not designed to trick learners, nor is it effortless. It requires understanding financial services regulation, ethical standards, mortgage products, and the application of advice principles at a professional level.

Which module feels hardest depends on individual strengths. For most learners, CeMAP feels hardest at the beginning, when everything is new. As knowledge builds, confidence usually increases.

The key factor is not natural intelligence or prior background. It is preparation, consistency, and engagement with the material.

With realistic expectations and structured study, the CeMAP exams are demanding but manageable.

Looking for training support?

We offer CeMAP training for learners working towards a career in mortgage advice. Our courses follow the London Institute of Banking & Finance syllabus and are designed to support understanding of mortgage regulation and advice requirements.

Explore our accredited CeMAP training courses

> Futuretrend Financial Training