Starting the Certificate in Mortgage Advice and Practice (CeMAP) can feel like opening a textbook that never seems to end. Many learners begin with enthusiasm, only to find themselves overwhelmed by the sheer volume of information. From financial regulations and mortgage products to legal principles and industry terminology, there is a lot to absorb.

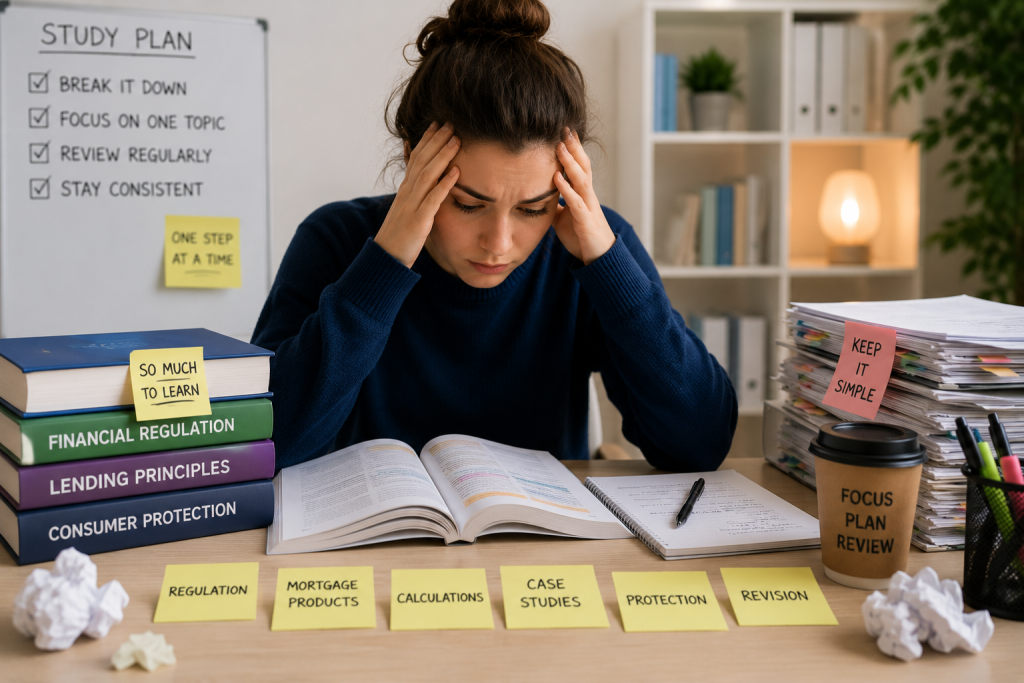

Information overload is one of the biggest reasons learners lose confidence early in their studies. Fortunately, it does not mean you’re incapable of passing CeMAP. It usually means you’re trying to learn too much at once.

Understanding why information overload happens, and having a simple way to manage it, can make studying feel far more achievable

Why Does CeMAP Feel Like Too Much Information?

Information overload happens when your brain receives more new information than it can comfortably organise and retain.

CeMAP introduces many concepts that are unfamiliar to people entering the mortgage industry. You’re not only learning facts but also understanding how different areas connect, including regulation, ethics, lending criteria, protection products and the wider financial services market.

Because everything feels new, it’s easy to think every sentence deserves equal attention. This often leads to reading pages repeatedly without remembering much afterwards.

The important thing to remember is that feeling overwhelmed is a normal part of learning something substantial. Your brain is building new knowledge rather than simply recalling familiar information.

What Makes CeMAP Content Feel So Overwhelming?

Several factors combine to create the feeling of overload.

Everything Appears Equally Important

When you’re new to CeMAP, it’s difficult to distinguish essential concepts from supporting detail. Without experience, every paragraph can seem equally critical.

Over time, patterns begin to emerge. Core principles are revisited throughout the qualification, while some supporting details simply provide context.

New Terminology Slows Learning

CeMAP introduces many financial and regulatory terms that most learners have never encountered before.

Every unfamiliar word requires extra mental effort to understand before you can even absorb the topic itself. Once this vocabulary becomes familiar, studying becomes much faster.

Trying to Learn Too Much in One Sitting

Many learners believe long study sessions produce better results. In reality, concentration naturally declines after extended periods.

Trying to complete multiple chapters in one evening often leaves you remembering very little by the end.

Shorter, focused sessions usually produce stronger understanding and better long-term memory.

How Do You Manage CeMAP Content Without Feeling Overwhelmed?

The simplest approach is to stop thinking about CeMAP as one large qualification.

Instead, think of it as hundreds of small learning tasks.

Rather than aiming to “study CeMAP tonight”, aim to understand one topic well.

For example:

- Mortgage regulation

- Types of repayment mortgages

- Interest calculations

- The house buying process

Completing one manageable topic provides a sense of progress without creating unnecessary pressure.

Small wins build confidence much more effectively than attempting huge amounts of reading.

Why Should You Break Topics Into Smaller Parts?

Breaking information into smaller sections reduces the amount your working memory has to process at once.

Instead of reading an entire chapter, divide it naturally into sections.

A simple approach might look like this:

- Read one small section.

- Summarise it in your own words.

- Test yourself without looking at your notes.

- Move on only when you understand the basic idea.

This keeps learning active rather than passive.

Understanding one topic thoroughly is more valuable than rushing through several chapters without retaining them.

How Do You Prioritise What to Learn?

Not every piece of information requires the same level of attention during your first study session.

A useful approach is to separate content into three categories.

Must Understand

These are the core principles that underpin multiple parts of CeMAP.

Examples include:

- FCA regulation

- Mortgage repayment methods

- Types of mortgage products

- Affordability principles

- Consumer protection

These topics deserve your greatest attention because they appear repeatedly throughout your studies.

Useful Supporting Knowledge

Some sections provide context that helps explain the bigger picture.

These are still important but become easier once you understand the core concepts first.

Fine Detail

Certain facts, figures or definitions can be refined during later revision.

Trying to memorise every detail on your first reading often causes unnecessary stress.

Building understanding before memorisation usually produces better exam preparation.

A Simple Framework for Managing CeMAP Content

You do not need complicated revision systems or expensive productivity apps.

A straightforward four-step framework is often enough.

Step 1: Choose One Topic

Avoid opening multiple modules at once.

Decide exactly what you’re studying before you begin.

Step 2: Understand Before Memorising

Focus on answering one question:

“Do I understand why this works?”

If the answer is yes, remembering the details becomes much easier later.

Step 3: Review Soon Afterwards

A short review later that day or the following day helps reinforce what you’ve learned before it begins to fade.

Frequent reviews are usually more effective than one long revision session weeks later.

Step 4: Move On Gradually

Once you’re comfortable with one topic, begin the next.

This steady approach creates lasting knowledge without overwhelming yourself.

Should You Study Everything Perfectly the First Time?

No.

One of the biggest causes of information overload is believing every page must be fully understood immediately.

Learning rarely works like that.

Most successful CeMAP learners revisit topics several times.

Each review strengthens understanding because you’re connecting new knowledge with concepts you’ve already learned.

Progress is built through repetition rather than perfection.

How Can You Tell If You're Experiencing Information Overload?

Common signs include:

- Reading the same paragraph repeatedly.

- Forgetting what you read a few minutes earlier.

- Feeling mentally exhausted after short study sessions.

- Jumping between multiple topics without finishing any.

- Feeling busy without making progress.

These signs usually indicate that it’s time to simplify your study approach rather than work harder.

Should You Take Breaks When Studying CeMAP?

Yes.

Learning depends on giving your brain time to process information.

Short breaks between focused study sessions help maintain concentration and reduce mental fatigue.

Stepping away for ten minutes after completing a topic is often far more productive than forcing yourself to continue when your concentration has dropped.

Consistency over several weeks is much more valuable than one exhausting day of revision.

Does Information Overload Get Better?

Yes.

As your understanding grows, new topics begin connecting with previous ones instead of feeling completely unfamiliar.

Financial terminology becomes easier.

Regulatory concepts become more familiar.

Mortgage products begin to make logical sense.

Many learners find that the first few weeks are the hardest because almost everything is new. Once you’ve established a solid foundation, learning generally becomes more manageable.

Frequently Asked Questions

How do I manage CeMAP content?

The most effective way to manage CeMAP content is to break it into small, manageable topics, focus on understanding core CeMAP concepts before memorising details, review regularly and study consistently rather than trying to learn large amounts in one sitting.

How many CeMAP topics should I study each day?

There is no perfect number. Many learners make better progress by focusing on one or two topics thoroughly instead of rushing through several chapters.

Is it normal to forget what I’ve studied?

Yes. Forgetting some information is a normal part of learning. Regular review helps strengthen memory and improves long-term understanding.

Should I make detailed notes on everything?

Not necessarily. Notes should help clarify key ideas rather than copy entire textbooks. Simple summaries written in your own words are often more useful than lengthy notes.

Final Thoughts

Information overload is one of the most common challenges faced by CeMAP learners, particularly during the early stages of study. It happens because you’re absorbing a significant amount of new information in a relatively short period, not because you’re incapable of learning it.

The key is to simplify your approach. Break large topics into smaller sections, focus on understanding before memorising, prioritise the most important concepts and review your learning regularly. Small, consistent steps almost always lead to better results than trying to master everything at once.

Remember that CeMAP is designed to build your knowledge over time. As your understanding develops, subjects that once felt overwhelming gradually become familiar, helping you study with greater confidence and less stress.

Looking for training support?

We offer CeMAP training for learners working towards a career in mortgage advice. Our courses follow the London Institute of Banking & Finance syllabus and are designed to support understanding of mortgage regulation and advice requirements.

Explore our accredited CeMAP training courses

> Futuretrend Financial Training