Virtual classroom learning has become one of the most popular ways to study for CeMAP. It offers the structure of live teaching while allowing learners to study from home or another convenient location. For many people, it provides a balance between the flexibility of online learning and the support of a traditional classroom.

However, simply attending the sessions is only part of the process. The learners who gain the most from a CeMAP virtual classroom course are usually those who prepare before each lesson, stay engaged during teaching and review what they have learned afterwards.

Whether you have already enrolled or are deciding if live online training is right for you, understanding how to use virtual classroom CeMAP training effectively can help you make the most of your investment of both time and effort. This approach aligns with best practices for educational, answer-led content and clear learner guidance.

What Is a CeMAP Virtual Classroom Course?

A CeMAP virtual classroom course is a live online training programme where an instructor teaches learners in real time using video conferencing software. Rather than watching pre-recorded videos whenever you choose, you join scheduled sessions alongside other learners.

The course typically follows a structured timetable, allowing tutors to explain key topics, answer questions and guide learners through the CeMAP syllabus.

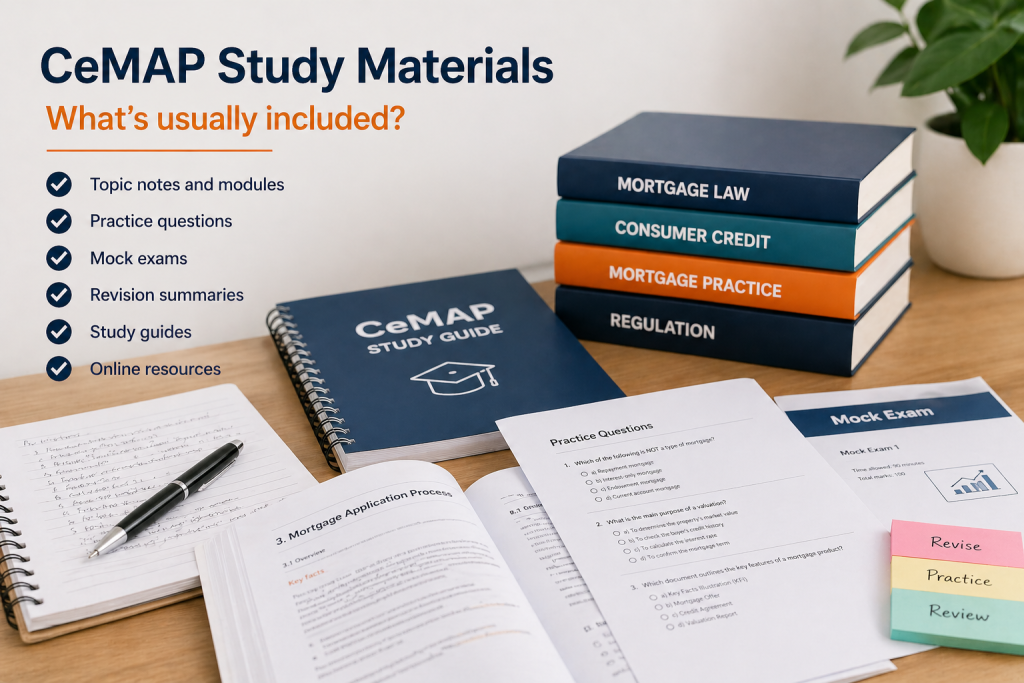

Most virtual classroom providers also include supporting resources such as:

- Digital course manuals

- Practice questions

- Revision materials

- Mock exams

- Tutor support between sessions

This combination of live teaching and independent study gives learners regular guidance while still allowing time to study between classes.

What Should You Expect from a CeMAP Virtual Classroom Session?

Knowing what happens during a session helps reduce uncertainty before your course begins.

Although every provider structures lessons slightly differently, most sessions follow a similar pattern.

A typical lesson may include:

- A review of previous topics

- Introduction of new learning outcomes

- Tutor explanations using presentations or examples

- Opportunities to ask questions

- Worked examples and practice questions

- Discussion of common exam misunderstandings

- Guidance on what to study before the next lesson

Rather than expecting to memorise everything during the live session, think of each class as building your understanding of the subject. Your own revision afterwards is what helps turn that understanding into exam knowledge.

How Should You Prepare Before Each Virtual Classroom Session?

Preparing before each lesson makes it much easier to follow the tutor and participate confidently.

Even spending 20 to 30 minutes beforehand can improve your understanding considerably.

Read Any Pre-Course Materials

Many training providers send course notes or reading materials before each lesson.

Having a basic awareness of the topic means you spend less time trying to understand unfamiliar terminology during the session and more time listening to the tutor’s explanations.

You do not need to master the content beforehand. Simply becoming familiar with the main concepts can make a noticeable difference.

Create a Suitable Study Environment

Virtual learning works best when you treat it like attending a physical classroom.

Choose somewhere:

- Quiet

- Comfortable

- Well lit

- Free from interruptions

- With a reliable internet connection

If possible, avoid studying from places where you are likely to become distracted, such as the living room while others are watching television.

A dedicated workspace also helps you mentally switch into study mode.

Check Your Technology Beforehand

Technical problems can interrupt learning unnecessarily.

Before your first session, check:

- Your internet connection

- Camera

- Microphone

- Speakers or headset

- Laptop charger

- Login details

Joining five or ten minutes early gives you time to resolve any problems before teaching begins.

How Can You Stay Engaged During Virtual Classroom CeMAP Training?

One of the biggest advantages of live online learning is the ability to interact with experienced tutors.

Taking an active role usually leads to better understanding than simply watching passively.

Ask Questions When Something Is Unclear

Many learners worry about asking questions because they think everyone else understands the topic.

In reality, other learners often have the same question.

Good tutors expect questions throughout the course and can often explain concepts in several different ways.

If something does not make sense, asking immediately is usually better than hoping it becomes clearer later.

Take Your Own Notes

Even if comprehensive course manuals are provided, writing your own notes helps reinforce learning.

Rather than copying every word from the presentation, focus on:

- Key definitions

- Important rules

- Areas you find difficult

- Tutor explanations that helped something make sense

These personalised notes often become some of your most useful revision resources later.

Minimise Distractions

Studying from home brings temptations that would not exist in a classroom.

Try to avoid:

- Checking emails

- Looking at social media

- Watching television

- Using your phone unnecessarily

- Working on unrelated tasks

Even brief interruptions can make it harder to follow detailed financial concepts.

Why Participation Matters More Than Attendance

Attending every session is important, but participation is what helps develop understanding.

Learners who contribute during discussions often remember information more effectively because they are actively processing what they hear.

Participation might include:

- Answering tutor questions

- Joining discussions

- Completing exercises

- Sharing your reasoning

- Asking for clarification

You do not need to speak constantly. Simply engaging with the learning process keeps your attention focused.

How Should You Review After Each Session?

One of the biggest mistakes learners make is assuming the live lesson is enough.

The most effective learning usually happens after the session ends.

Review Your Notes the Same Day

Revisiting your notes while the lesson is still fresh helps strengthen your memory.

Even a short review can identify areas that need further study before they become larger problems.

Review Your Notes the Same Day

Revisiting your notes while the lesson is still fresh helps strengthen your memory.

Even a short review can identify areas that need further study before they become larger problems.

Complete Practice Questions

CeMAP examinations test how well you understand the syllabus rather than whether you attended lessons.

Practice questions help you:

- Apply your knowledge

- Identify weak areas

- Become familiar with exam wording

- Build confidence gradually

If you answer questions incorrectly, use them as learning opportunities rather than signs of failure.

Organise Your Revision

After each lesson, organise your notes alongside your course materials.

Keeping everything clearly labelled makes later revision much easier.

Many learners use folders or digital note systems organised by CeMAP unit, allowing them to find information quickly when preparing for exams.

Should You Study Between Virtual Classroom Sessions?

Yes. Independent study is an important part of every CeMAP virtual classroom course.

Live sessions introduce and explain topics, but personal study helps reinforce and retain that knowledge.

Between lessons, you could:

- Re-read course materials

- Complete practice questions

- Review tutor notes

- Create revision summaries

- Revise difficult topics

- Test yourself using flashcards

Studying little and often is generally more effective than leaving everything until just before the exam.

What Are the Most Common Mistakes Learners Make?

Understanding common mistakes can help you avoid unnecessary difficulties during your course.

Expecting the Tutor to Do All the Learning

Tutors explain complex topics clearly, but learning still requires personal effort.

Virtual classroom training works best when learners actively revise outside scheduled sessions.

Falling Behind After Missing One Lesson

Life sometimes gets in the way, and missing a session does not automatically mean you cannot succeed.

The important thing is catching up promptly by reviewing recordings if available, reading the course materials and speaking with your tutor if necessary.

Leaving gaps for several weeks often makes later topics much harder to understand.

Ignoring Areas That Feel Difficult

It can be tempting to focus on subjects you already understand.

Instead, spend additional time on weaker topics while tutor support is still available.

Addressing small misunderstandings early is usually much easier than revisiting them shortly before the exam.

Not Using Available Support

Many virtual classroom providers offer additional support beyond the live lessons.

This may include tutor email access, revision sessions, discussion groups or extra learning resources.

Making use of these opportunities can help clarify difficult topics and maintain momentum throughout the course.

Is Virtual Classroom Learning Right for Everyone?

Not necessarily.

Some learners enjoy the flexibility and interaction of live online teaching, while others may prefer self-paced study or traditional classroom learning.

Virtual classroom courses often suit learners who:

- Like structured study schedules

- Benefit from live explanations

- Want opportunities to ask questions

- Appreciate regular accountability

- Prefer learning from home

Those who need complete flexibility because of unpredictable work patterns may find on-demand online learning more suitable.

Choosing the right format depends on your learning style, availability and personal preferences rather than one method being better than another.

How to Use Virtual Classroom CeMAP Training Successfully

Getting the most from a CeMAP virtual classroom course is about more than simply logging in each day. Preparing before lessons, engaging during teaching and reviewing afterwards all contribute to stronger understanding and greater confidence.

The live sessions provide valuable structure, guidance and opportunities to ask questions, but they work best when combined with regular independent study. Treat each lesson as part of an ongoing learning process rather than a standalone event.

With consistent preparation, active participation and steady revision, virtual classroom training can provide an effective route towards achieving your CeMAP qualification while giving you the support of experienced tutors and fellow learners throughout your studies.

Looking for training support?

We offer CeMAP training for learners working towards a career in mortgage advice. Our courses follow the London Institute of Banking & Finance syllabus and are designed to support understanding of mortgage regulation and advice requirements.

Explore our accredited CeMAP training courses

> Futuretrend Financial Training

One of our past learners recently became a finalist in the

One of our past learners recently became a finalist in the