Starting CeMAP can feel like a big step, especially if you are new to financial services. Most learners focus on how to revise or which course to choose, but there are a few basics that matter just as much and are often missed at the start.

This guide answers a simple but important question: what should you know before starting CeMAP? Getting these foundations right can make your study smoother, more manageable, and far less frustrating.

What is CeMAP and why does it matter?

CeMAP is the industry standard qualification for mortgage advisers in the UK. It is awarded by the London Institute of Banking & Finance and meets the Financial Conduct Authority education requirements for giving mortgage advice.

It matters because without it, you cannot legally advise on mortgages in the UK. It is not just a course. It is the starting point for a regulated career.

That context is important. You are not just studying to pass exams. You are learning knowledge that underpins real financial decisions for clients.

1. CeMAP is manageable, but it is not “easy”

A lot of learners ask whether CeMAP is difficult. The honest answer is that it is very manageable with the right approach, but it is not something you can rush through without effort.

Why this matters

Some learners start thinking it will be straightforward because it is an entry-level qualification. Others go the opposite way and assume it will be overwhelming.

Both views can cause problems:

- Underestimating it leads to poor preparation

- Overestimating it leads to unnecessary stress

The reality sits in the middle. The content is clear and structured, but there is quite a lot of it.

What to expect

CeMAP is split into three modules:

- CeMAP 1 focuses on regulation and core financial services knowledge

- CeMAP 2 covers mortgage products and processes

- CeMAP 3 applies your knowledge through case studies

Each builds on the last. If you take shortcuts early on, it tends to catch up with you later, especially in CeMAP 3.

A steady, consistent approach works far better than trying to cram.

2. How you study matters as much as what you study

There is no single “best” way to study CeMAP. Some learners prefer structured lessons, others prefer self-paced learning.

Why this matters

Many learners struggle not because the content is too hard, but because their study method does not suit them.

For example:

- Reading alone may not work if you need explanation

- Videos alone may not stick without practice questions

- Intensive courses may feel too fast if you need time to absorb topics

Practical advice

Before you start, think about:

- How you usually learn best

- How much time you can realistically commit each week

- Whether you need structure, flexibility, or a mix of both

Many learners benefit from combining resources. For example:

- Study materials that break down the syllabus

- Videos explaining each topic

- Practice questions to check understanding

- Mock exams to get used to the format

The key point is this: your study method should support your learning, not work against it.

3. Time management is one of the biggest challenges

One of the most common issues learners face is not difficulty with the content, but difficulty staying consistent.

Why this matters

CeMAP is often studied alongside:

- Full-time work

- Family commitments

- Other responsibilities

Without a plan, it is easy to fall behind or lose momentum.

What works in practice

You do not need a perfect timetable. You need a realistic one.

A simple approach:

- Break the syllabus into smaller sections

- Set weekly goals rather than vague intentions

- Build in time for revision and practice exams

It is also worth accepting that some weeks will not go to plan. That is normal. The important thing is to get back on track rather than stopping altogether.

Consistency over time matters far more than short bursts of heavy studying.

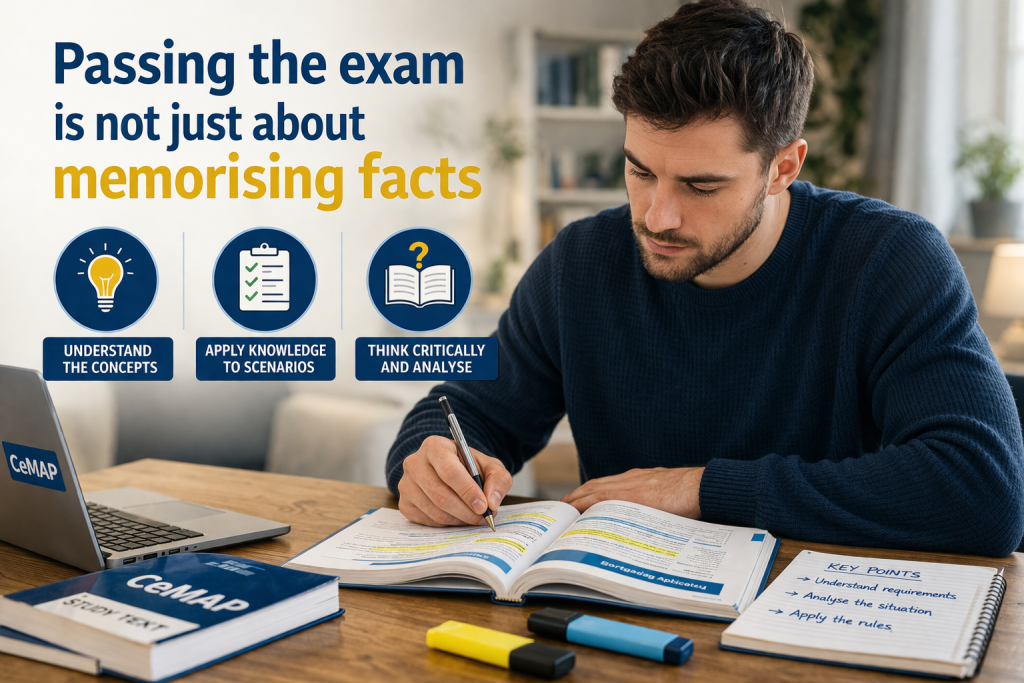

4. Passing the exam is not just about memorising facts

It is easy to assume that CeMAP is mainly about remembering information. In reality, understanding is just as important.

Why this matters

The exams, particularly later modules, test how well you can apply knowledge, not just recall it.

For example:

- Understanding why a regulation exists

- Knowing how a mortgage product fits a situation

- Interpreting information in a case study

Common mistake

A common mistake is relying too heavily on reading or passive learning without testing yourself.

This often leads to a situation where:

- The content feels familiar

- But confidence drops in the exam

Better approach

Use a mix of:

- Topic-based questions after each section

- Regular recap of key areas

- Full mock exams to simulate the real experience

Practising exam-style questions is one of the most effective ways to build confidence and identify gaps.

5. Support and structure can make a big difference

Not all learners need the same level of support, but having access to guidance can make the process smoother.

Why this matters

Studying alone can work well for some people, but others benefit from:

- Being able to ask questions

- Having topics explained in different ways

- Staying accountable to a study plan

Without support, it is easier to feel stuck or lose direction.

What to look for

Effective support does not have to be complicated. It can include:

- Clear study materials that simplify the syllabus

- Access to tutors or learning support teams

- Structured learning paths

- Practice resources aligned with the exam format

Some learners prefer virtual classrooms for structure, while others prefer flexible home study with support available when needed.

There is no right or wrong choice. It depends on what helps you stay consistent and confident.

How do these five points fit together?

Each of these insights connects to the same idea:

Success in CeMAP is less about ability and more about preparation and approach.

If you:

- Understand what the qualification involves

- Choose a study method that suits you

- Manage your time realistically

- Focus on understanding, not just memorising

- Use support where needed

You give yourself a much stronger starting point.

What should you know before starting CeMAP?

Before you begin, you should know that:

- CeMAP is a structured but manageable qualification

- Your study approach will shape your experience

- Time management is key to staying on track

- Exams test understanding as well as knowledge

- The right level of support can make a real difference

These are not complicated ideas, but they are often overlooked. Getting them right early can save time, reduce stress, and improve your chances of progressing smoothly through the qualification.

Final thoughts

Starting CeMAP is a practical step towards a regulated career, not just an academic exercise. That is why it is worth approaching it with a clear plan rather than rushing in.

You do not need to have everything figured out from day one. Most learners adjust their approach as they go. What matters is starting with a realistic view of what is involved and giving yourself the structure to succeed.

If you go in with the right expectations and a steady approach, CeMAP becomes far more straightforward than many people expect.

Looking for training support?

We offer CeMAP training for learners working towards a career in mortgage advice. Our courses follow the London Institute of Banking & Finance syllabus and are designed to support understanding of mortgage regulation and advice requirements.

Explore our accredited CeMAP training courses

> Futuretrend Financial Training