Choosing how to study for CeMAP is one of the first real decisions you make on the path to becoming a mortgage adviser. The two most common routes are online learning and classroom-based learning, including virtual classrooms.

Both can work. Neither is automatically better. The difference comes down to how the training is structured and how well it fits your time, learning style, and support needs.

This guide explains how each method works, where each one helps, and how to decide what suits you.

What is CeMAP and how is it typically studied?

CeMAP (Certificate in Mortgage Advice and Practice) is the industry standard qualification for mortgage advisers in the UK. It is awarded by the London Institute of Banking & Finance (LIBF) and meets the Financial Conduct Authority (FCA) education requirements for giving mortgage advice.

You can study CeMAP in several ways:

- Fully online through structured learning platforms

- Virtual classroom sessions with live tutors

- In-person classroom courses

- A blended approach combining all three

Most modern CeMAP training programmes combine elements of online study with tutor support, rather than relying on a single format.

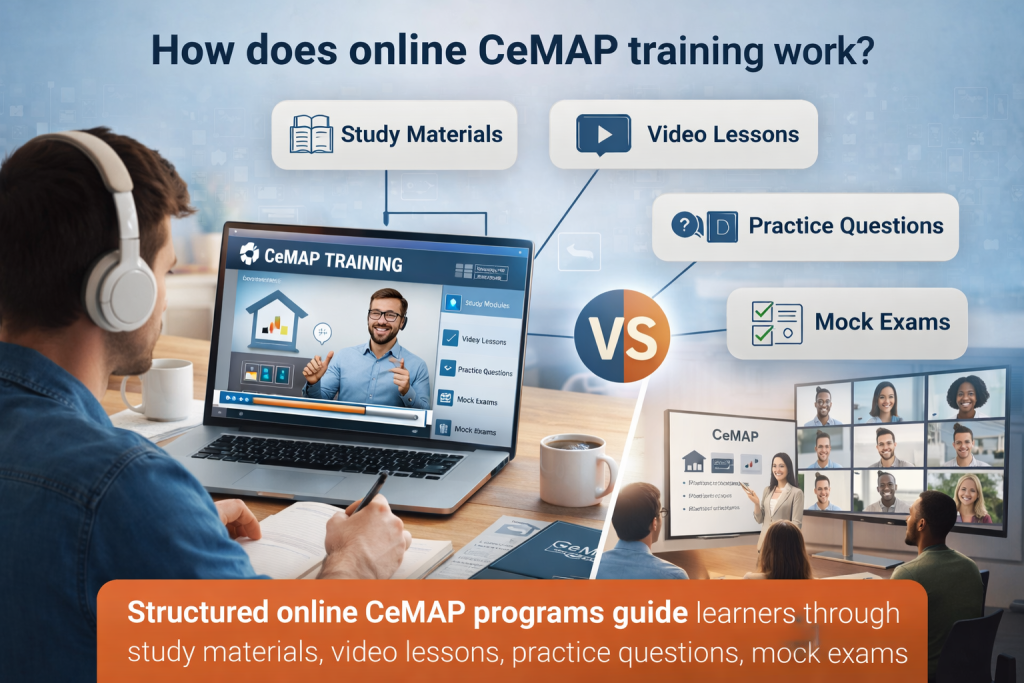

How does online CeMAP training work?

Online CeMAP training is typically delivered through a digital learning platform. This is often referred to as a home study or self-paced course.

A well-structured online programme usually includes:

- Study materials that break down the syllabus into manageable topics

- Video lessons explaining key concepts

- Topic-based questions to test understanding

- Mock exams and LIBF specimen papers

- Recaps and summaries to reinforce learning

- Ongoing updates aligned with syllabus changes

The key point is structure. Online learning is not just reading a textbook. The more effective programmes guide you through the syllabus step by step.

Many learners use platforms that include full study support resources such as topic walkthroughs, exam-style questions, and revision tools designed to mirror the CeMAP exam format.

What are the advantages of online CeMAP training?

Online learning can be very effective when it is used properly.

Flexibility around your schedule

You can study at times that suit you. This is especially useful if you are working, changing careers, or balancing other commitments.

Control over pace

You can spend longer on difficult topics and move quickly through areas you already understand. This is often important in CeMAP 1, where financial regulation can take time to absorb.

Repeatable learning

You can revisit videos, notes, and questions as many times as needed. This helps reinforce understanding rather than relying on memory from a single session.

Continuous access to resources

Good online CeMAP training platforms provide ongoing access to materials, meaning you can revise whenever needed rather than relying on fixed course dates.

Lower barriers to entry

Online training often removes travel and scheduling constraints, making it easier to start studying sooner.

That said, flexibility can also be a drawback if it leads to inconsistency.

What are the limitations of online learning?

Online CeMAP training is only as effective as the structure and discipline behind it.

Requires self-motivation

Without fixed sessions, it is easy to delay studying or lose momentum. This is one of the most common reasons learners struggle.

Less immediate interaction

If you are unsure about a topic, you may not get an instant explanation unless support is built into the course.

Risk of passive learning

Watching videos or reading notes does not always translate into exam readiness. Active practice through questions and mock exams is essential.

Can feel isolating

Some learners prefer discussion and interaction, especially when working through complex areas like mortgage products or case study scenarios in CeMAP 3.

This is why many online programmes now include additional support layers such as tutor access or virtual classrooms.

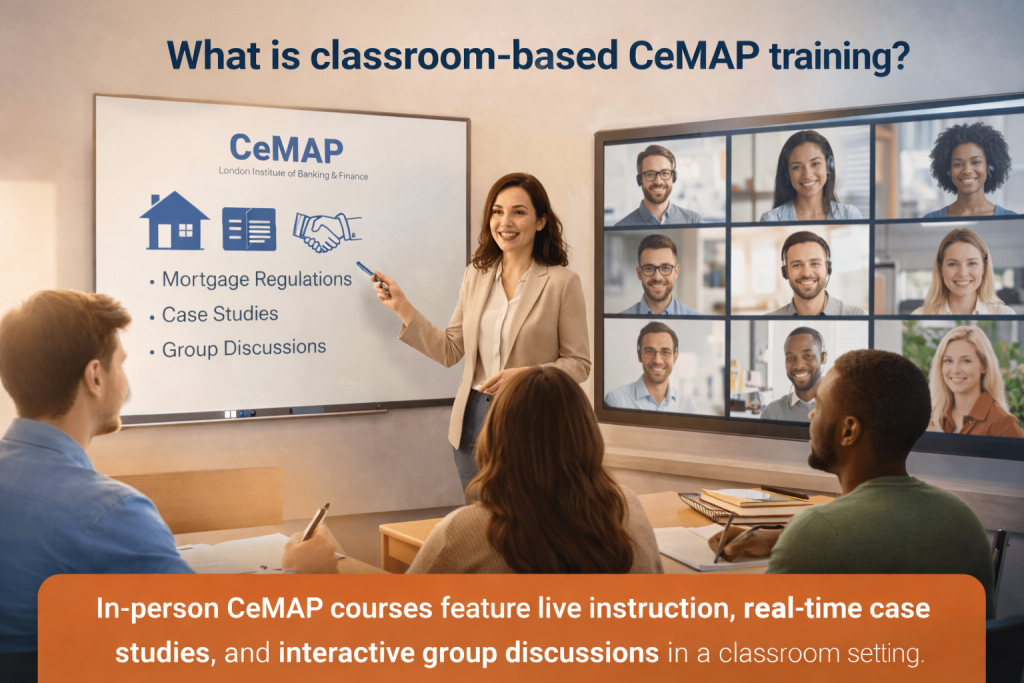

What does structured learning actually look like?

Classroom-based training involves learning in a structured environment, either in person or through a live virtual classroom.

Traditional classroom learning usually includes:

- Scheduled sessions led by a tutor

- Group discussions and interaction

- Real-time explanations and examples

- A fixed pace covering the syllabus

Virtual classroom training follows a similar structure but is delivered online through live sessions rather than in a physical location.

Many CeMAP providers now offer virtual classrooms with smaller groups, allowing learners to ask questions and engage with the tutor while still studying remotely.

What are the benefits of classroom and virtual classroom learning?

Classroom-style learning offers a different type of support.

Structured schedule

You follow a set timetable, which helps maintain consistency and progress.

Immediate clarification

You can ask questions and get answers straight away, which is useful for more complex topics.

Guided learning

The tutor controls the pace and ensures key areas are covered thoroughly.

Accountability

Attending sessions creates a sense of commitment, which can help learners stay on track.

Peer interaction

Learning alongside others can help reinforce understanding and highlight different ways of approaching questions.

Virtual classrooms offer many of these benefits while removing the need to travel.

What are the limitations of classroom-based learning?

Classroom training is effective, but it is not always the best fit for everyone.

Fixed pace

You move at the speed of the group. If you fall behind or already understand a topic, it can feel restrictive.

Less flexibility

You must attend at specific times, which may not suit work or personal commitments.

Limited repetition

Once a session is finished, you cannot always revisit it unless recordings or additional materials are provided.

Travel (for in-person courses)

Attending physical classes may involve time and cost that not all learners can accommodate.

Because of this, many learners combine classroom sessions with online resources to reinforce learning.

Is online CeMAP training any good?

Yes, online CeMAP training can be very effective, but only when it is structured properly and used consistently.

The quality of the programme matters more than the delivery method.

A strong online course should:

- Follow the full LIBF syllabus clearly

- Break topics into manageable sections

- Include exam-style questions and mock tests

- Provide explanations, not just information

- Support different learning styles through varied content

When these elements are in place, many learners perform just as well as those in classroom settings.

However, if the course lacks structure or the learner struggles with self-discipline, progress can slow down.

How does virtual classroom learning bridge the gap?

Virtual classroom learning sits between fully online and traditional classroom study.

It combines:

- The structure of scheduled sessions

- Live tutor interaction

- The convenience of studying from home

Many CeMAP learners use virtual classrooms alongside online study platforms. For example, they may:

- Study topics independently using structured online materials

- Attend live sessions to reinforce understanding

- Use tutor sessions to clarify difficult areas

This blended approach is becoming more common because it supports both flexibility and structure.

Which learning method suits different types of learners?

The best method depends on how you learn and how you manage your time.

Online learning often suits learners who:

- Prefer studying at their own pace

- Are comfortable learning independently

- Need flexibility around work or family commitments

- Like revisiting material multiple times

Classroom or virtual classroom learning often suits learners who:

- Prefer structured schedules

- Benefit from live explanations

- Like asking questions in real time

- Stay motivated through routine and accountability

There is no right or wrong choice. The key is being honest about what helps you stay consistent and engaged.

Does the learning method affect exam success?

The method itself does not determine whether you pass CeMAP exams.

What matters more is:

- How well you understand the syllabus

- How much practice you do with exam-style questions

- How familiar you are with the exam structure

- How consistently you study

For example:

- A learner using a structured online CeMAP training platform with regular practice may perform better than someone attending classroom sessions without revising properly.

- Equally, a learner who benefits from tutor guidance may progress faster in a virtual classroom environment.

Both routes can lead to the same outcome if used effectively.

How important is structure in CeMAP training?

Structure is one of the most important factors in successful CeMAP study.

Regardless of whether you choose online or classroom learning, your training should:

- Follow a clear path through the syllabus

- Build knowledge step by step

- Include regular knowledge checks

- Prepare you for exam-style questions

- Reinforce learning through repetition

Many modern CeMAP training programmes are designed with this in mind, combining:

- Structured study materials

- Video explanations

- Topic-based questions

- Mock exams

- Tutor support

This kind of approach is often more important than whether the delivery is online or in a classroom.

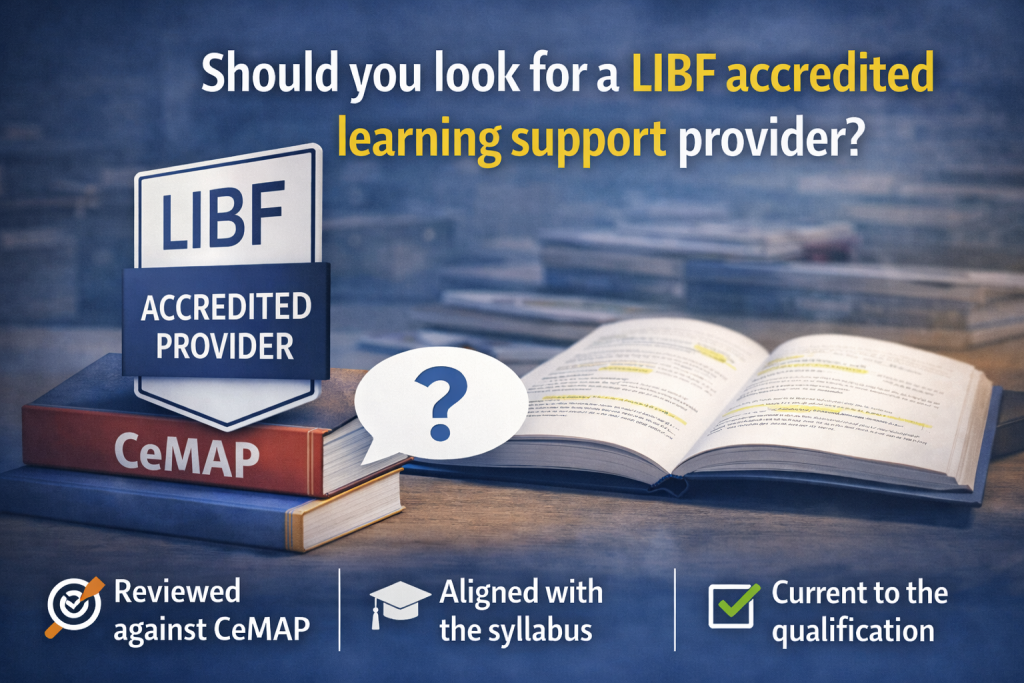

Should you look for a LIBF accredited learning support provider?

Yes, and many learners do.

A combined approach might include:

- Studying core topics through an online learning platform

- Attending virtual classroom sessions for key areas

- Using mock exams and question banks for revision

- Accessing tutor support when needed

This allows you to benefit from both flexibility and structured guidance.

It also reflects how many learners naturally study. Few rely on a single method throughout the entire CeMAP journey.

Final thoughts

Online CeMAP training is effective when it is structured, supported, and used consistently. Classroom and virtual classroom learning are effective when they provide clarity, guidance, and accountability.

The real difference is not the format, but how well the method fits you.

If you need flexibility and control, online learning can work very well.

If you prefer structure and interaction, classroom-style learning may suit you better.

If you want both, a blended approach often provides the best balance.

Most importantly, focus on how you learn, not just how the course is delivered. The right structure, resources, and consistency will always matter more than the format alone.

Looking for training support?

We offer CeMAP training for learners working towards a career in mortgage advice. Our courses follow the London Institute of Banking & Finance syllabus and are designed to support understanding of mortgage regulation and advice requirements.

Explore our accredited CeMAP training courses

> Futuretrend Financial Training