Becoming a mortgage adviser does not follow a single fixed timeline. For most people, it involves three main stages: gaining the required qualification, becoming authorised through a firm, and building experience in the role. Each stage takes a different amount of time depending on your circumstances, pace of study, and the route you take into the industry.

This guide explains what actually happens at each stage and why the overall timeline can vary quite a lot from one person to another.

How long does the qualification stage take?

The first step is gaining a recognised qualification that meets regulatory requirements. In the UK, this is typically CeMAP (Certificate in Mortgage Advice and Practice).

For many learners, the qualification stage takes several months, but this is not fixed.

Some key factors that affect how long this stage takes:

Study pace

If you are studying alongside a full-time job or other commitments, progress will usually be slower. Learners who study more intensively can move through the material more quickly, but that depends on availability and confidence with exams.

Previous knowledge

If you already have experience in financial services, you may find parts of the content more familiar. If you are completely new to the industry, you may need more time to understand the terminology and concepts.

Exam readiness

Passing the exams is not just about reading. Many learners need time to practise applying knowledge, not just recognising it. This often extends the timeline beyond what people expect at the start.

A realistic way to view this stage is not as a race, but as a period of building a solid foundation. Rushing through it can make later stages harder.

What happens after you pass CeMAP?

Passing the qualification does not mean you can immediately start advising clients.

You must work under an authorised firm, and that firm is responsible for ensuring you are competent before you advise customers independently.

This stage is often referred to as authorisation, onboarding, or competency sign-off.

How long does it take to get authorised?

There is no single timeframe for authorisation because it depends heavily on the firm you join.

Most firms will require:

- Initial training on their systems and processes

- Understanding of compliance and regulation

- Supervised practice before advising independently

- Demonstration of competence

This process can take weeks to several months, depending on:

The firm’s structure

Some firms have formal training academies with structured timelines. Others take a more gradual, on-the-job approach.

Your starting point

If you are new to financial services, there may be more to learn before you are ready to advise. If you already have relevant experience, progression may be quicker.

Your starting point

If you are new to financial services, there may be more to learn before you are ready to advise. If you already have relevant experience, progression may be quicker.

Compliance requirements

Mortgage advice is regulated, so firms must be confident you can give suitable advice. This is not something that can be rushed.

A key point here is that authorisation is not just a box to tick. It is about proving you can apply knowledge safely in real situations.

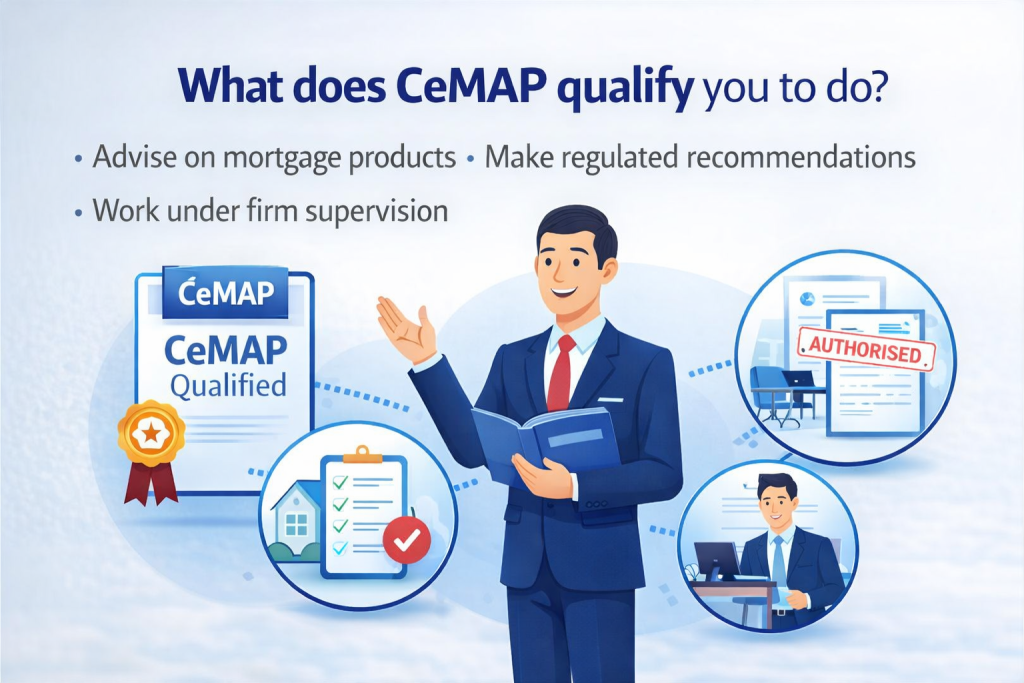

What does “competent adviser status” mean?

A mortgage adviser is usually considered fully operational once they are signed off as competent by their firm.

This means they can:

- Advise clients without supervision

- Recommend suitable mortgage products

- Follow regulatory and compliance standards

Reaching this stage takes time because it involves real client interaction, not just theory.

Many new advisers underestimate how different real-world advice is compared to studying.

How long does it take to feel confident in the role?

Even after becoming authorised, there is still a learning curve.

In the early months, advisers are often:

- Building confidence in client conversations

- Learning how to gather accurate information

- Understanding lender criteria in practice

- Managing application processes

It is common for this stage to take several more months before things start to feel natural.

Confidence develops through repetition and experience, not just training.

What does a typical overall timeline look like?

While there is no fixed timeline, a broad structure often looks like this:

- Qualification: several months

- Authorisation and onboarding: a few months

- Early experience and confidence building: ongoing

In total, becoming fully comfortable in the role can take many months to over a year.

That does not mean you are not working during that time. It means you are developing into the role gradually.

Why do timelines vary so much?

One of the most common questions people ask is why timelines differ so widely. The answer is that becoming a mortgage adviser depends on more than just passing exams.

Personal circumstances

Study time, work commitments, and learning pace all affect how quickly you move through the qualification stage.

Career background

Someone coming from a financial services role may progress differently to someone changing careers entirely.

Type of employer

Different firms have different onboarding processes. Some move quickly, others focus on longer development periods.

Learning style

Some people prefer to take time to fully understand topics, while others move faster but may need to revisit areas later.

Confidence and communication

Mortgage advice involves working with people, not just numbers. Developing communication skills can take time, especially if it is new to you.

Because of these factors, two people starting at the same point can reach the same role at very different speeds.

Can you speed up the process?

It is possible to move more quickly through certain stages, but there are limits.

You can:

- Study more consistently

- Use a mix of learning methods, not just reading

- Practise exam-style questions

- Prepare for interviews and job applications early

However, you cannot skip:

- Regulatory requirements

- Competency assessments

- Real-world experience

Trying to rush through these areas can make the transition into the role more difficult later on.

Is there a “fast track” route?

Some training providers or employers describe fast-track routes into mortgage advice.

These usually mean:

- Structured CeMAP study programmes

- Direct pathways into employment

- Intensive training schedules

While these can reduce downtime between stages, they do not remove the need for:

- Passing exams

- Demonstrating competence

- Gaining experience

So while the structure may feel quicker, the core steps remain the same.

What should you focus on instead of time?

A better question than “How quickly can I become a mortgage adviser?” is:

“How well prepared will I be when I get there?”

Focusing only on speed can lead to:

- Gaps in knowledge

- Low confidence in client situations

- Difficulty applying theory in practice

Focusing on preparation helps you:

- Understand the material properly

- Build confidence gradually

- Transition more smoothly into the role

In the long run, this often leads to better outcomes than trying to move as quickly as possible.

What is the realistic expectation?

A realistic expectation is that becoming a mortgage adviser is a process, not a single step.

It includes:

- Learning the knowledge

- Proving competence

- Applying that knowledge in real situations

Each stage builds on the previous one.

Most people do not become fully confident advisers overnight. They develop into the role over time.

Final thoughts

So, how long does it take to become a mortgage adviser?

The honest answer is that it depends, but it is rarely immediate. For most people, it takes several months to gain the qualification, followed by further time to become authorised and confident in the role.

There is no standard timeline because the journey depends on your background, your pace, and the path you take into the industry.

What matters most is not how quickly you reach the role, but how prepared you are when you do. A steady, well-understood progression tends to lead to a stronger and more sustainable career.

Looking for training support?

We offer CeMAP training for learners working towards a career in mortgage advice. Our courses follow the London Institute of Banking & Finance syllabus and are designed to support understanding of mortgage regulation and advice requirements.

Explore our accredited CeMAP training courses

> Futuretrend Financial Training