If you’ve decided to study for CeMAP, one of the first choices you’ll face is deciding which training provider to use. A quick online search reveals dozens of companies offering CeMAP courses, all claiming to help you succeed.

So how do you know which CeMAP provider is best?

The honest answer is that there isn’t one provider that’s automatically the best for everyone. The right choice depends on how you learn, the level of support you want, your available study time and what you expect from your training.

While price often catches people’s attention first, it rarely tells the whole story. A cheaper course can end up costing more if it lacks support or leaves you needing additional resources later. Equally, the most expensive provider isn’t necessarily the best fit either.

This guide explains the key factors to compare so you can choose a CeMAP training provider based on quality, transparency and overall value rather than simply the lowest price. It follows best practice for clear, answer-led educational content.

Which CeMAP Provider Is Best?

The best CeMAP provider is the one that offers the right balance of high-quality learning materials, experienced tutor support, flexible study options and clear guidance throughout your studies. Rather than focusing only on cost, compare how each provider helps learners understand the syllabus and prepare for the exams.

When comparing providers, ask yourself:

- Will this course suit the way I learn?

- Is help available if I get stuck?

- Are the study materials up to date?

- Is everything included in the price?

- Can I see examples before I buy?

These questions often reveal far more than the headline price.

What Should You Compare Between CeMAP Training Providers?

Although providers all teach the same qualification, the learning experience can vary considerably.

The most useful comparisons include:

Quality of Study Materials

Good CeMAP learning materials should explain concepts clearly rather than simply repeat the official syllabus.

Look for resources that include:

- Clear explanations in plain English

- Worked mortgage examples

- Practice questions

- Mock exams

- Revision summaries

- Progress tracking

The aim is not simply to provide information but to help you understand it.

If the sample materials feel confusing or overly technical, studying the full course may become much harder than necessary.

Tutor Support

Support is one of the biggest differences between providers.

Some learners rarely need help, while others benefit from being able to ask questions when they become stuck.

Consider:

- Can you contact tutors directly?

- How quickly do they normally respond?

- Are there scheduled support sessions?

- Can you ask unlimited questions?

- Is support available throughout the course?

Having access to knowledgeable tutors can save hours of frustration and prevent small misunderstandings becoming bigger problems.

Learning Format

Everyone learns differently.

Some people enjoy studying independently, while others stay motivated through structured teaching.

Common learning formats include:

Self-study

Ideal for independent learners who want maximum flexibility.

Virtual live classes

Online sessions with tutors that provide structure while allowing you to study from home.

Classroom training

Face-to-face teaching over a set timetable with direct interaction.

Many providers also offer blended learning, combining live tuition with online resources and self-study.

Rather than asking which format is “best”, think about which one fits your schedule and learning style.

Why Does Tutor Experience Matter?

Experienced tutors often explain difficult topics more simply because they understand where learners commonly struggle.

This doesn’t necessarily mean they have been teaching for decades. Instead, look for providers whose tutors:

- Understand the CeMAP syllabus thoroughly

- Can explain complex topics clearly

- Encourage questions

- Keep course content current

- Have experience supporting adult learners

Teaching ability is just as important as subject knowledge.

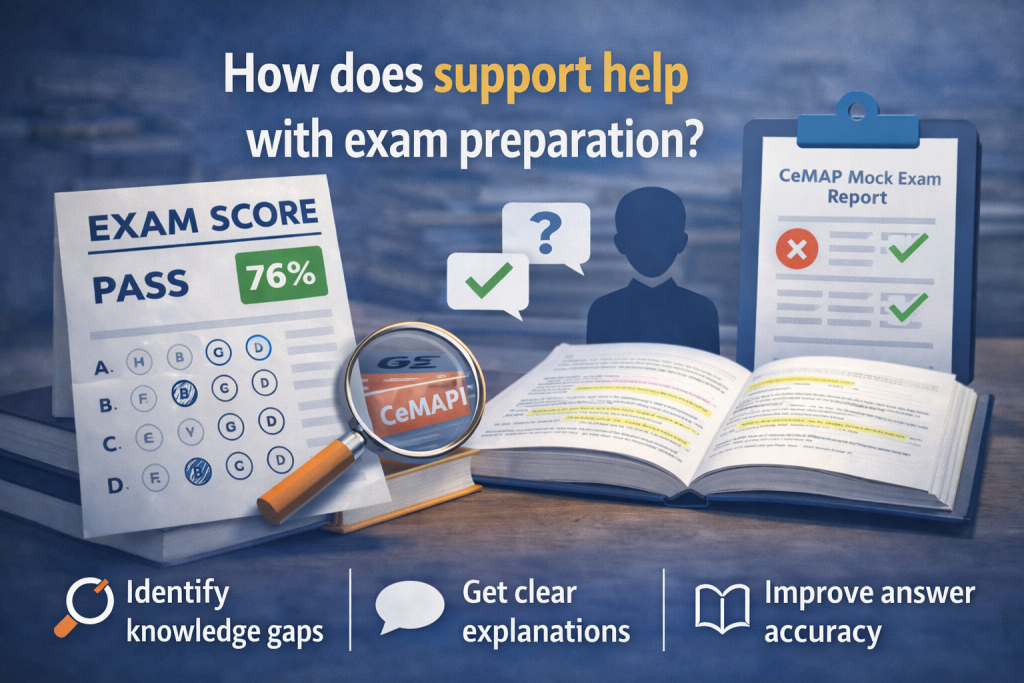

Are Practice Questions and Mock Exams Important?

Yes.

Reading course notes alone is rarely enough preparation for CeMAP exams.

Practice questions help you:

- Apply what you’ve learned

- Identify weak areas

- Become familiar with question styles

- Build confidence before sitting the real exam

Mock exams are especially valuable because they recreate exam conditions and highlight topics that need further revision.

Providers offering a wide range of realistic practice questions often give learners better opportunities to test their understanding before exam day.

Should You Choose the Cheapest CeMAP Course?

Not necessarily.

A lower price may represent excellent value, but only if the course includes everything you need.

Sometimes lower-cost courses exclude:

- Tutor support

- Revision resources

- Mock exams

- Updated materials

- Additional learning aids

If you later need to buy extra resources or seek additional tuition, the overall cost may end up being higher.

Instead of asking, “Which course is cheapest?”, ask, “What am I getting for my money?”

That simple change in mindset often leads to a better long-term decision.

What's the Difference Between Price and Value?

Price is simply the amount you pay.

Value is what you receive in return.

Two providers might charge similar fees while offering very different learning experiences.

For example, one course might include:

- Live tutor sessions

- Comprehensive study manuals

- Video lessons

- Practice exams

- Ongoing learner support

Another may provide only downloadable notes with little or no assistance.

The second option may appear cheaper, but the first could offer considerably better value if it improves your understanding and confidence.

Looking beyond the initial price often helps you make a more informed decision.

Why Is Transparency Important?

Good training providers are open about what they offer.

Before enrolling, you should be able to find clear information about:

- Course content

- Study methods

- What’s included

- Support availability

- Expected study commitment

- Costs

If important information is difficult to find or seems unclear, it’s reasonable to ask questions before committing.

Transparent providers usually make it easier for learners to understand exactly what they’re purchasing.

Should Providers Offer Course Previews?

Course previews can be extremely helpful.

Many reputable providers allow prospective learners to view sample CeMAP materials, watch introductory videos or explore demonstrations of their learning platform.

A preview lets you judge:

- Whether the explanations make sense to you

- The quality of the learning materials

- How easy the platform is to use

- Whether the teaching style suits you

Since everyone learns differently, seeing part of the course before buying can make choosing much easier.

What Are the Warning Signs of a Poor Training Provider?

Not every provider offers the same level of quality.

While no single issue automatically means a provider should be avoided, several warning signs deserve careful consideration.

These include:

Unrealistic Promises

Be cautious of claims that suggest guaranteed exam passes, guaranteed careers or exceptionally quick qualification with little effort.

CeMAP requires genuine study, and no provider can guarantee individual outcomes.

What Are the Warning Signs of a Poor Training Provider?

Not every provider offers the same level of quality.

While no single issue automatically means a provider should be avoided, several warning signs deserve careful consideration.

These include:

Unrealistic Promises

Be cautious of claims that suggest guaranteed exam passes, guaranteed careers or exceptionally quick qualification with little effort.

CeMAP requires genuine study, and no provider can guarantee individual outcomes.

Lack of Clear Information

If it’s difficult to discover:

- what’s included,

- who provides support,

- how learning works, or

- what happens after enrolment,

it may be harder to know exactly what you’re paying for.

Outdated Course Information

Financial regulation and qualification content can change over time.

Training providers should clearly maintain and update their learning materials when necessary.

Studying from outdated content can create unnecessary confusion.

Limited Ways to Get Help

If support is only available through slow or restricted channels, learners may struggle when they need clarification.

Reliable communication is often an important part of successful study.

Poor Reviews Without Context

Reviews should never be the only deciding factor.

Instead of focusing on overall ratings alone, read comments carefully.

Look for repeated themes such as:

- quality of support

- responsiveness

- organisation

- learning experience

Every provider will receive occasional negative feedback, but consistent patterns can

Should Online Reviews Influence Your Decision?

Reviews can help, but they shouldn’t make the decision for you.

People are more likely to leave reviews after either extremely positive or extremely negative experiences.

Instead, combine reviews with other evidence, including:

- course previews

- available support

- study resources

- transparency

- learning format

- your own preferences

Taking a balanced view usually leads to a better decision than relying solely on ratings.

Does the Learning Platform Matter?

Absolutely.

If you’ll be studying CeMAP online for several weeks or months, you’ll spend a lot of time using the provider’s learning platform.

A good platform should make studying easier by offering:

- simple navigation

- clear lesson structure

- progress tracking

- mobile compatibility where appropriate

- easy access to learning resources

A confusing platform can make studying feel more difficult than it needs to be.

Questions to Ask Before You Enrol

Before making your final decision, consider asking:

- What support is included?

- Are study materials updated regularly?

- Are mock exams included?

- Can I study at my own pace?

- Is there a course demonstration available?

- What happens if I need additional help?

- Are there any additional costs?

The answers should help you compare providers fairly.

Final Thoughts

Choosing a LIBF CeMAP training provider isn’t about finding the cheapest course or the company making the biggest promises. It’s about finding the learning experience that gives you the best chance of understanding the material, staying motivated and preparing confidently for your exams.

The strongest providers are usually transparent about what they offer, provide high-quality study resources, make support readily available and help learners understand the qualification rather than simply memorise it.

By comparing structure, resources, support and overall value, you can make a decision based on what will genuinely help you succeed.

After all, investing in the right learning experience from the beginning can make your CeMAP journey smoother, more enjoyable and ultimately more rewarding.

Looking for training support?

We offer CeMAP training for learners working towards a career in mortgage advice. Our courses follow the London Institute of Banking & Finance syllabus and are designed to support understanding of mortgage regulation and advice requirements.

Explore our accredited CeMAP training courses

> Futuretrend Financial Training