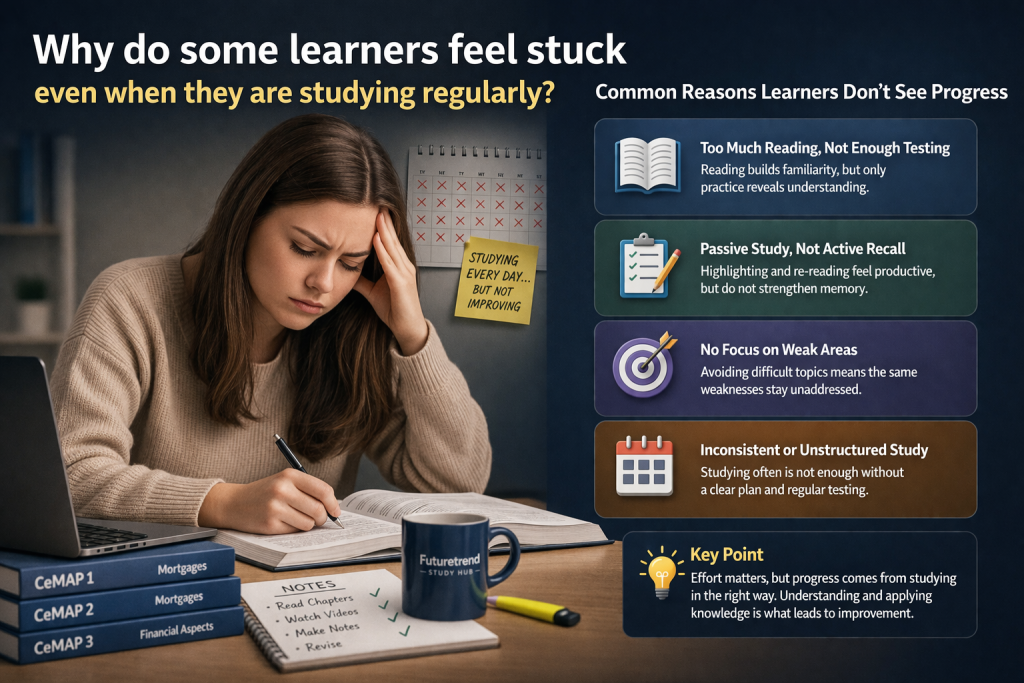

One of the biggest challenges for people studying CeMAP is not understanding the content. It is staying consistent over several weeks or months.

Many learners begin with enthusiasm, buy their study materials, create a timetable and promise themselves they will study every evening. Then life gets in the way. Work becomes busy, family commitments take priority or motivation fades after the first few chapters.

The good news is that consistency does not require perfect discipline. In fact, most successful CeMAP learners are not studying for hours every day. Instead, they develop realistic habits that fit around their lives and help them make steady progress.

If you’ve been wondering, “How do I stay consistent with CeMAP study?”, the answer usually lies in creating manageable routines rather than expecting yourself to study whenever motivation appears.

Why Does Consistency Matter More Than Studying for Long Hours?

Consistency is usually more effective than occasional bursts of intensive revision because learning happens over time.

CeMAP introduces a large amount of new terminology, regulation and mortgage knowledge. Trying to absorb everything in a single weekend often leads to information overload and poor retention.

Regular study sessions help you:

- Build knowledge gradually

- Improve long-term memory

- Spot weaker topics earlier

- Feel more confident before exams

- Reduce last-minute stress

Many learners believe they need marathon revision sessions to succeed. In reality, studying for 45 to 90 minutes several times each week is often far more productive than studying for six hours once a fortnight.

The goal is to keep moving forward, even if progress sometimes feels slow.

Why Do So Many Learners Lose Momentum?

Losing motivation is completely normal during a longer qualification.

CeMAP covers three modules and a wide range of subjects. After the excitement of starting fades, learners often experience periods where studying feels more like a chore.

Common reasons include:

- Feeling overwhelmed by the amount of content

- Trying to study when mentally tired

- Missing a few planned sessions and feeling guilty

- Comparing progress with other learners

- Having no clear study routine

Missing one study session is rarely the problem. The bigger issue is convincing yourself that you’ve “fallen behind” and giving up altogether.

Instead, view every study session as a fresh start.

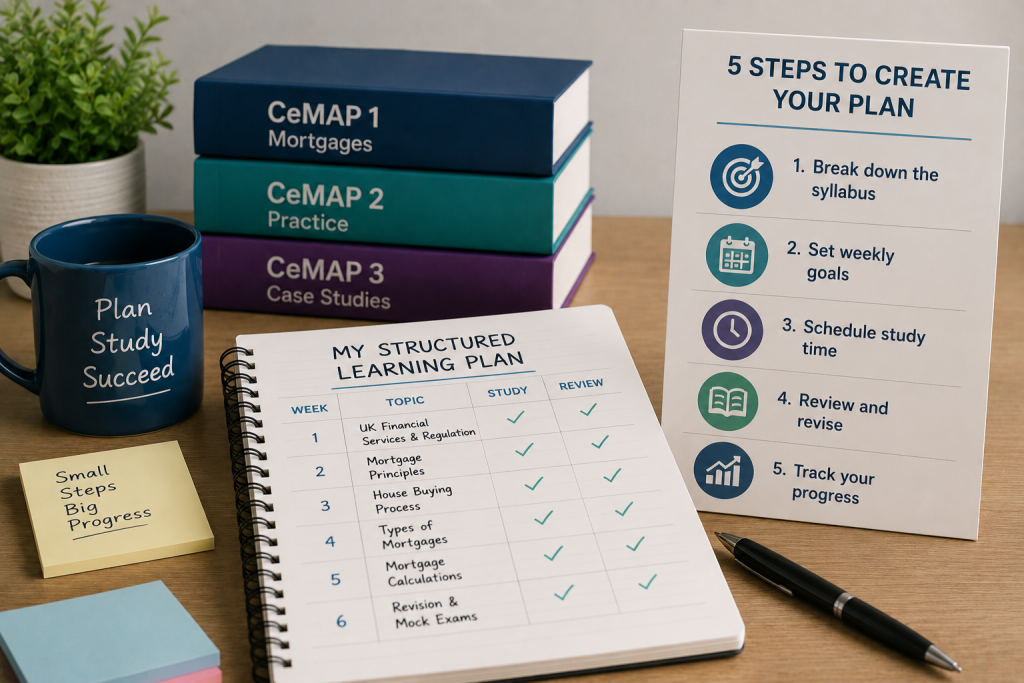

What Does a Realistic CeMAP Study Routine Look Like?

There is no perfect timetable that works for everyone.

Your study routine should fit around your existing responsibilities rather than compete with them.

For someone working full time, a realistic week might look like:

Day | Study Activity |

Monday | 60 minutes reading and note-taking |

Tuesday | Evening off |

Wednesday | 60 minutes video lesson or revision |

Thursday | 45 minutes practice questions |

Friday | Evening off |

Saturday | 90 minutes covering a new topic |

Sunday | 60 minutes reviewing the week’s learning |

This provides around five hours of focused study each week without requiring every evening to be dedicated to CeMAP.

Some learners prefer studying early in the morning, while others concentrate better after work. The best routine is the one you can realistically maintain.

How Can You Make Studying Easier to Start?

One of the biggest obstacles is simply getting started.

When a study session feels overwhelming, your brain naturally looks for something easier to do.

A simple way to overcome this is to reduce the barrier to beginning.

For example:

- Leave your study materials ready the night before.

- Decide exactly which topic you’ll study.

- Set a timer for just 20 minutes.

- Put your phone somewhere out of reach.

- Begin with a quick review of your previous session.

Once you’ve started, continuing often becomes much easier.

Many learners find that motivation follows action rather than the other way around.

Which Study Methods Help Maintain Consistency?

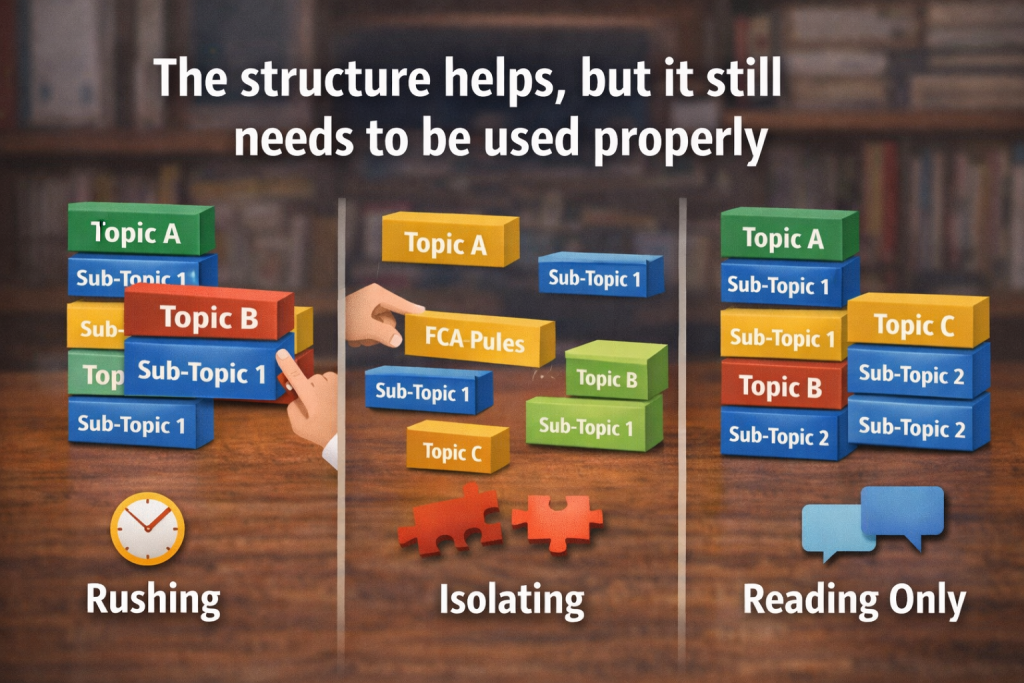

Using the same CeMAP study method every time can become repetitive.

Changing how you learn while keeping the study habit consistent can help maintain interest.

For example, you might alternate between:

- Reading the course manual

- Watching tutor-led videos

- Completing practice questions

- Creating flashcards

- Explaining topics aloud in your own words

- Reviewing previous exam questions

Using different approaches also helps reinforce learning from multiple angles.

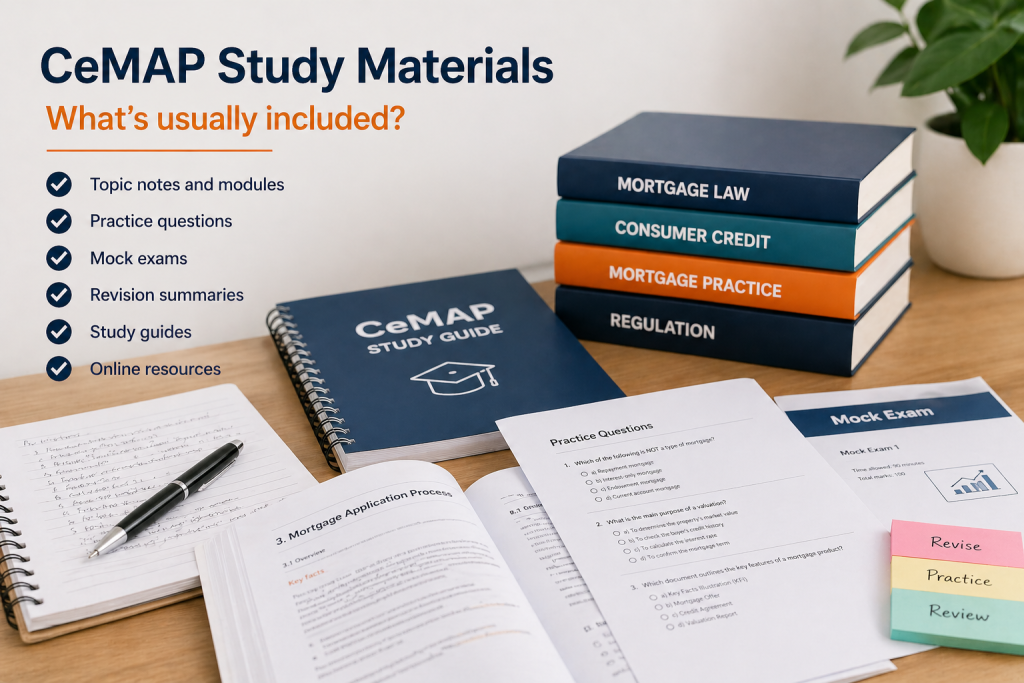

If you’re using additional resources, make sure they come from an accredited CeMAP learning support provider recognised by the London Institute of Banking & Finance. Accurate, up-to-date materials can make revision more effective and help avoid confusion caused by unofficial or outdated content.

How Can You Avoid Common Distractions?

Modern distractions are everywhere.

Phones, social media, emails and streaming services can quickly turn a planned one-hour study session into ten minutes of actual learning.

Simple changes can make a significant difference:

- Silence phone notifications.

- Study away from the television.

- Close unnecessary browser tabs.

- Tell family members when you’ll be studying.

- Keep only the materials you need on your desk.

You do not need a perfect home office.

A quiet, organised space that signals “study time” is usually enough.

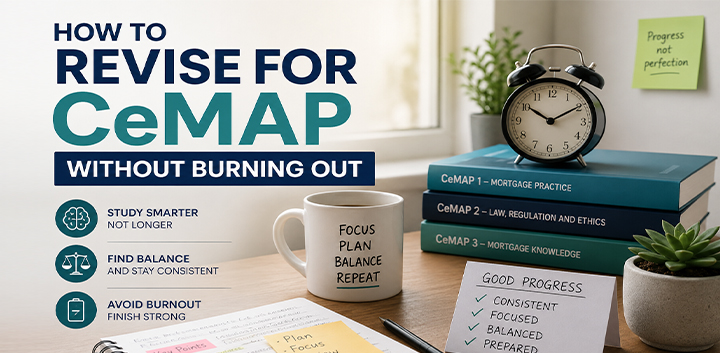

Should You Study Every Day?

Not necessarily.

Studying every day works well for some people but can become difficult to maintain alongside work and personal commitments.

Planned rest days are often beneficial.

Taking breaks helps prevent burnout and gives your brain time to process new information.

A routine that you can maintain for three months is far more valuable than an ambitious schedule that only lasts one week.

Remember that consistency means showing up regularly, not constantly.

How Do You Stay Motivated When Progress Feels Slow

Progress during CeMAP is not always obvious.

There may be weeks where you feel like you’re forgetting more than you’re learning.

This is a normal part of studying complex material.

Instead of focusing on how much remains, look at what you’ve already completed.

Some helpful ways to stay motivated include:

- Crossing completed chapters off a checklist

- Tracking practice exam scores

- Setting small weekly goals

- Celebrating completing each module

- Remembering why you started

Breaking larger goals into smaller milestones makes progress feel more achievable.

Is It Better to Study Alone or With Support

Both approaches can work well.

Some learners enjoy studying independently because they can work at their own pace.

Others find that regular support helps them remain accountable.

Support might include:

- Tutor-led virtual classroom sessions

- Classroom training

- Online learner communities

- Study partners

- Tutor feedback sessions

Having someone to ask questions or explain difficult topics can prevent small problems from becoming larger obstacles.

Many learners also find that scheduled lessons naturally encourage consistency because they provide fixed points in the week.

What Should You Do If You Fall Behind?

Almost every CeMAP learner misses study sessions at some point.

The important thing is how quickly you restart.

Avoid trying to “catch up” by doubling your study hours.

Instead:

- Accept that the missed session has gone.

- Review where you stopped.

- Continue with your normal routine.

- Adjust your weekly plan if necessary.

Missing a few days does not undo everything you’ve already learned.

Consistency is built over months, not individual evenings.

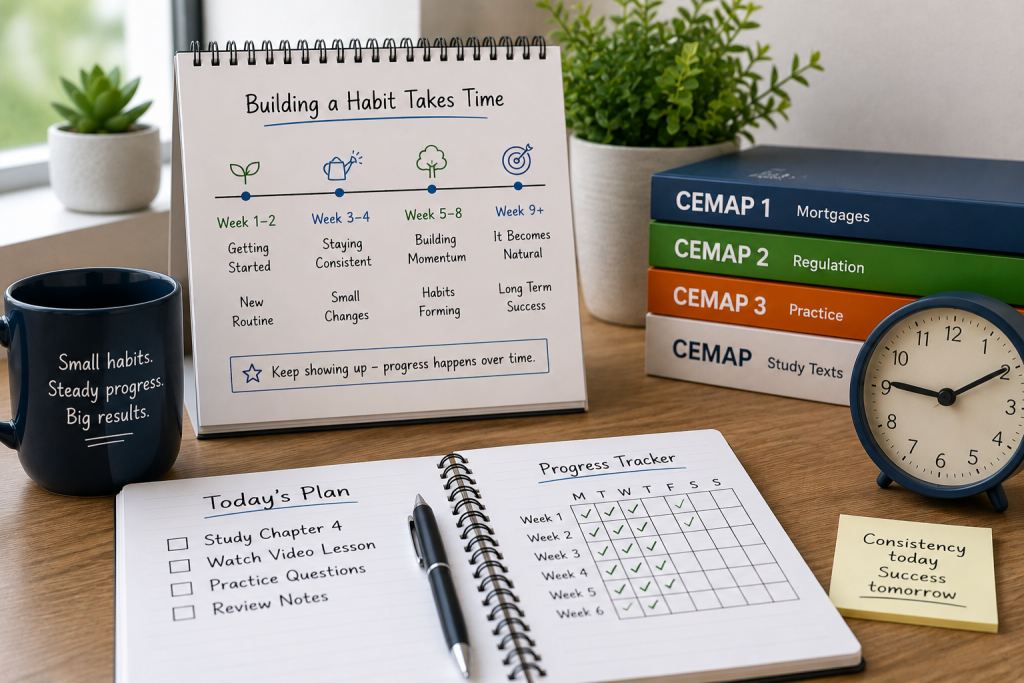

How Long Does It Take to Build a Consistent Study Habit?

Some people settle into a routine within a couple of weeks, while others take longer to find a pattern that suits their lifestyle.

The important thing is to make studying part of your normal weekly routine rather than waiting until you feel motivated.

Treat your study sessions like any other appointment. When they become a regular part of your week, keeping momentum becomes much easier.

Even short, focused sessions completed consistently can lead to significant progress over time.

Frequently Asked Questions

How do I stay consistent with CeMAP study?

Stay consistent by creating a realistic weekly routine that fits around your existing commitments. Short, regular study sessions are usually more effective than occasional long revision days. Reducing distractions and setting small weekly goals can also help you maintain momentum.

How many hours a week should I study for CeMAP?

There is no set number of hours that suits everyone. Many learners make steady progress by studying around five to eight hours each week, depending on their previous knowledge, learning style and available time.

What if I miss a week of studying?

Missing a week is not a failure. Review the last topic you covered, refresh your understanding and continue with your normal study plan. Avoid trying to make up all the missed time in one go, as this can lead to burnout.

Is studying little and often better for CeMAP?

Yes. Regular study sessions generally improve understanding and memory more effectively than occasional intensive revision. Consistent learning also makes it easier to retain the large amount of information covered throughout the qualification.

Final Thoughts

Staying consistent with CeMAP is less about finding the perfect study plan and more about developing habits you can realistically maintain.

Small, regular study sessions often produce better results than relying on motivation or last-minute revision. By creating a routine that fits your lifestyle, reducing distractions and accepting that occasional setbacks are normal, you give yourself the best chance of making steady progress.

The learners who succeed are rarely those who study the hardest every single day. More often, they are the ones who keep showing up, week after week, until they reach the finish line.

Looking for training support?

We offer CeMAP training for learners working towards a career in mortgage advice. Our courses follow the London Institute of Banking & Finance syllabus and are designed to support understanding of mortgage regulation and advice requirements.

Explore our accredited CeMAP training courses

> Futuretrend Financial Training